Ladies and gentlemen, it’s now official – there is a fix for the family glitch.

If an employer makes an offer of health insurance coverage to an employee’s spouse or dependent(s) that is deemed unaffordable by a federal standard, then that spouse, and/or dependent(s) are free to shop for individual coverage on healthcare.gov. That lets them qualify to draw down premium tax credits that help pay for their coverage, if they are eligible based on their income.

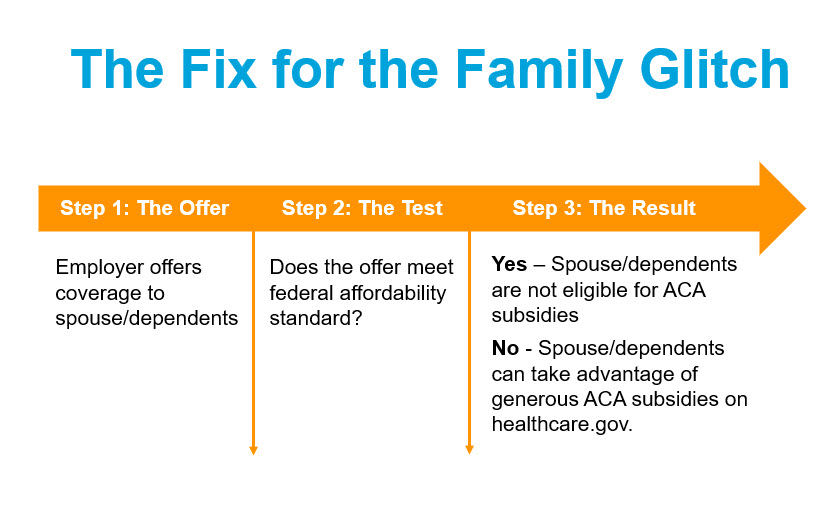

What Was the Glitch?

Since 2010, spouses and dependents were blocked from getting access to generous advanced tax credit subsidies to help pay for health plan premiums because of the mere fact that an employer made them an offer through the employee in their family. The employer’s offer could be terrible, unaffordable, very expensive, but none of that mattered in the past. Until now, the mere existence of an employer’s offer blocked the dependents from drawing financial assistance through healthcare.gov.

The IRS has been working all year to re-write that rule. I’ve seen the final version, and it is in place for all health plan coverage effective on Jan. 1, 2023, and beyond.

What does this look like in real life? Imagine I have a job and my employer offers me health insurance for myself, my spouse and my children. My coverage costs him $700 a month, and he is willing to subsidize 80% of that, so I’m left only paying $140/month as my share. He also offers coverage to my family (let’s say a spouse and two children under age 19) at an additional cost of $1,400 a month. BUT he is unwilling to subsidize that coverage at all.

In other words, to cover my spouse and children, I’d have had to foot the entire $1,400-a-month bill. And, to make matters worse, my spouse and children are not eligible to shop for individual health insurance on healthcare.gov and draw down tax credits to help pay the premiums, no matter how low our household income is. That’s been the situation for the past 12 years.

What’s the Fix?

It’s a new day starting on Jan. 1, 2023.

That’s when that offer of coverage by my employer for my spouse’s and children’s health care coverage can be compared to a new standard: 9.12% of my household income. So, if we take that $1,400 and annualize it, that means I would pay$16,800 a year out of my pocket to provide insurance for my wife and children through my employer plan. But what if my household income was $100,000 per year? Is his offer affordable then, under the new rule?

Nope. He would have to come in under $9,120 a year ($760/month) to be considered affordable for my family under this new standard. This means my wife and kids get to go to healthcare.gov and shop for individual coverage, using whatever premium tax credits they qualify for to help our family pay for it. And as we’ve discussed, premium tax credits from now through 2025 are the highest they’ve ever been. VERY generous!

The three steps in the fix for the family glitch

This is a major policy change. One that will provide more affordable health insurance coverage for millions of Americans who are struggling financially now because of an employer who is unwilling or unable to offer affordable health insurance. Here in Louisiana, I would not be surprised to see more than half of all employers’ dependent coverage falling into the “unaffordable” range. Not surprised at all.

Do the Math, Then Get Shopping

A couple of things to note:

- The affordability test is based on HOUSEHOLD income, not just the income of the employee whose employer is offering coverage.

- Dependents are people whom you claim as dependents on your taxes. To learn more about that, see this answer from the IRS.

The Straight Talk is, if you are suffering from very unaffordable dependent or spouse coverage today, you should be contacting an agent (at www.bcbsla.com) or 1-844-GET-BLUE (1-844-438-2583; TTY 711) and exploring your options for shopping on healthcare.gov starting Nov. 1. It costs NOTHING to allow these seasoned professionals to guide you and your family as you figure out how much premium tax credit you are entitled to under this new rule. The federal government will be making tens of billions of dollars available every year for this program; make sure your plan coverage is in place to start on Jan. 1, 2023. Don’t miss it!

Is the employer penalized for dependent (spouse/child(ren) coverage not meeting the affordability test? I don’t see how am employer would know what the employee’s “household” income is.

Thanks

Lori! Thanks for reaching out!

While employers retain their responsibility under the ACA to provide affordable coverage for their EMPLOYEES (assuming the employer is large, an ALE, over 50 FTE’s), they are not responsible for the affordability of the offer they MUST make under the law to dependents of their employees. That’s the beauty of this new rule, employers won’t be required to comply with anything new, and if their offer doesn’t pass the affordability test, the dependents can simply go to Healthcare.gov and shop there.

Also keep in mind that multiple offers apply. That is, an offer of coverage to dependents from EITHER spouse’s workplace must be tested and considered. If EITHER of those offers meets affordability requirements under the Family Glitch Fix, then those dependents are NOT eligible to go to Healthcare.gov and get subsidies. So both offer (if there are two of them) must be tested.

Great question!….mrb

Mike,

After your StraightTalk last week I sent this info out to some of my employees I think this will apply to and they have lots of questions I can’t answer. Maybe you can: 1) How is this household income going to be verified, etc. on the website? Is this going to be based on 2022 income, 2021 income, etc. via tax returns or exactly how? Or does the employee just certify an amount and then it’s verified later after taxes are filed? 2) With medicaid in LA planning to start recertifying people, what if someone gets kicked off medicaid in May, will they be able to go to Marketplace then?

Interesting that one of the biggest problems with the Marketplace when ObamaCare came out was all the sick people went there to get coverage which was a big drain and why a lot of insurers got out. So now, I guess the theory here is to get in most cases a younger, healthier group of dependents in the market?

Matt! Thanks for reaching out! That’s a lot of questions! While I’m not an accountant or attorney, I can help you find the answers to some of these questions.

1. When you shop on Healthcare.gov today, you are asked to make a good faith estimate of what your household income is going to be for the remainder of that calendar year. If you miss the number, you will reconcile it when you file your taxes. So if you over-estimate your income, you may be owed tax credits when you file. Likewise, if you under-estimate your income, you might find yourself with a bill from the IRS when you file. So tread carefully.

2. Losing affordable health insurance coverage has always been a special enrollment trigger for Healthcare.gov

3. I can’t comment on what “theory” that Marketplace might be operating on, I can only observe that the opportunity for Louisiana citizens to get the absolute best deals on health insurance is the best I’ve ever seen, and about to get even better!

Cheers!…mrb