Healthcare.Gov Pricing Under ARPA21

When I was a young man, around 15-years-old, I already had two jobs. One working at a tennis pro shop, stringing rackets, scheduling courts, teaching lessons, and selling equipment and clothing. The other job was working in a small convenience store, where I was clearly too young to do what the job required, but the owners loved having me around. I was in high school, but I was making a TON of money by mid-70s standards. So much, in fact, that I invested in a very nice stereo I bought out of the Sears catalog.

It had everything, 8-track player, turntable, AM/FM radio, and two separate speakers you could move apart from where you were sitting to get that maximum stereo effect! So cool!

In the package with the owner’s manual was a flier about a membership in something called the Columbia Record Club: “For just one cent, choose any 10 8-tracks or albums on this page and we’ll ship them out to you immediately!” Then, in the fine print at the bottom, “Simply purchase eight more tapes or albums at regular club prices over the next two years to complete your membership!” Sounded really great! I immediately picked out my 10 free 8-tracks (maybe two of which I actually wanted).

Soon, I began to realize a few things. Like “regular club prices” were roughly double what music cost in a shop back then. And every month, they would send a postcard and if you didn’t send it back right away, BAM, tapes, albums and the bills for them would start showing up at your door! And it didn’t stop when you bought your “eight more tapes or albums,” either! They kept coming until the entire two years was up!

You can’t escape “Dad Wisdom”

I complained constantly about it, until one day my Dad sat me down, looked me in the eye and said, “Boy, you’ve just learned an important lesson. Two, actually! First, there ain’t no free lunch! And second, if it sounds too good to be true, it almost always is!” I love my Dad, but THAT did not make me feel better. But of course, he was right. Almost always.

That’s why, when I began to read the American Rescue Plan Act of 2021 (ARPA 21), especially the section on the new Advanced Tax Credits (ATCs) for people shopping on healthcare.gov, I got really skeptical. The new ATCs were HUGE. The income caps we’d lived with for over a decade? GONE! The restrictions on purchasing coverage outside open enrollment? GONE! Wide-open enrollment, all the way until Aug. 15, 2021! It was like everything Dad warned me about, all in one place.

So, I dug, and I dug, and I dug, and April 1 rolled around (the posted effective date for all the new money and rules), and EVERYTHING I had heard or read about came true.

All of it. As of right now, and all the way until at LEAST Dec. 31, 2022, billions more dollars have been made available for people buying individual health insurance on healthcare.gov.

So, Mike, what does all this money do to premiums?

So glad you asked! I’ve created a couple of graphs because in this case, pictures really ARE worth a thousand words. These graphs anticipate that a single person would buy a silver plan in Baton Rouge’s 70810 ZIP code at various ages and incomes, which you’ll see as we go along. Note that all of the prices in these graphs are for 2021 premiums.

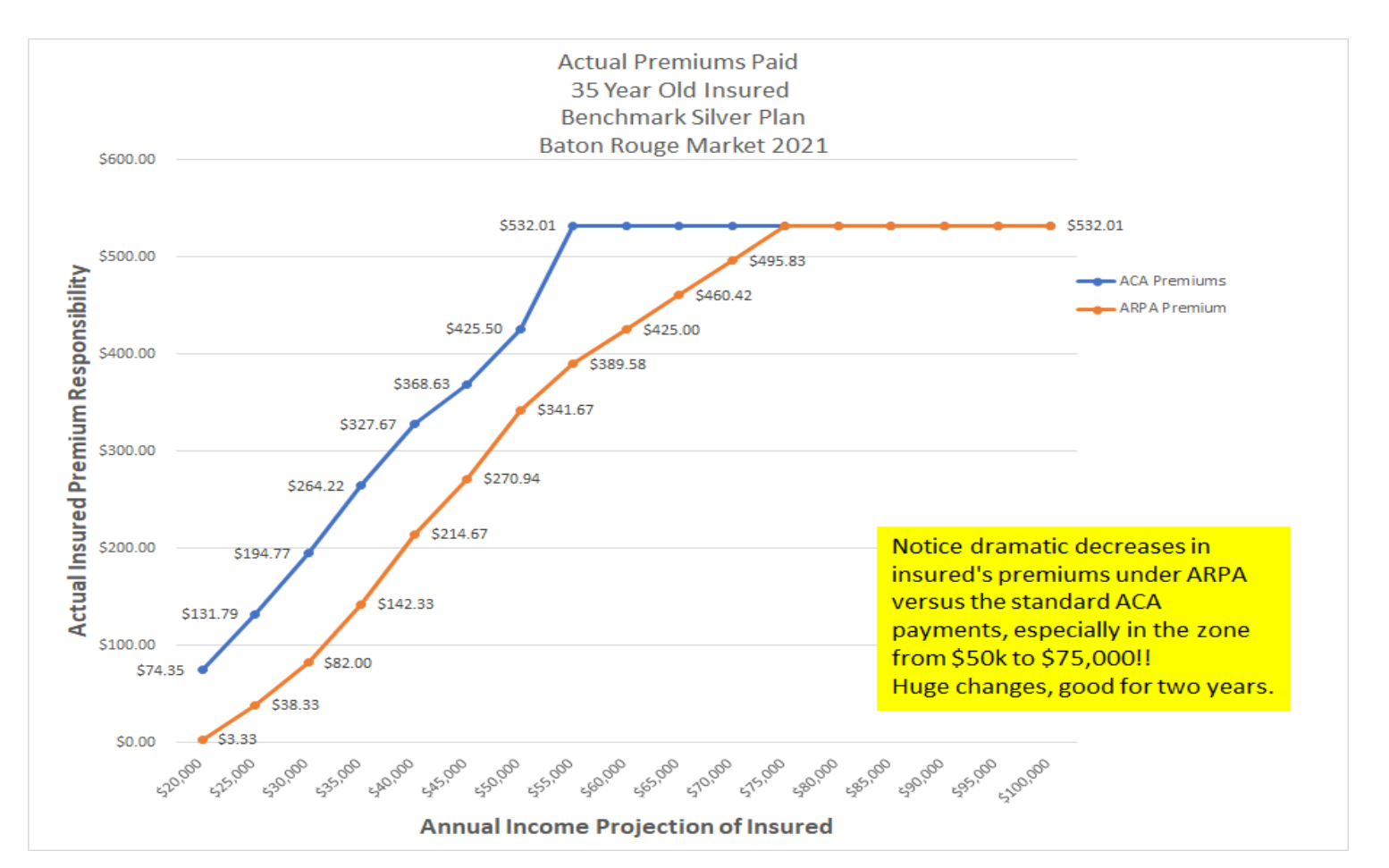

First, let’s check out the new pricing for a 35-year-old. In this graph, the blue line shows the old premiums under the original ACA pricing. The orange line shows the NEW pricing for the exact same coverage under the ARPA 21 rules. Under the old ACA rules, there was no financial help once your income hit 400% of the Federal Poverty Level (about $50k/year for a single). As you can see below, the part of the premium you are responsible for is noticeably lower in the new model, all the way to $75,000 per year.

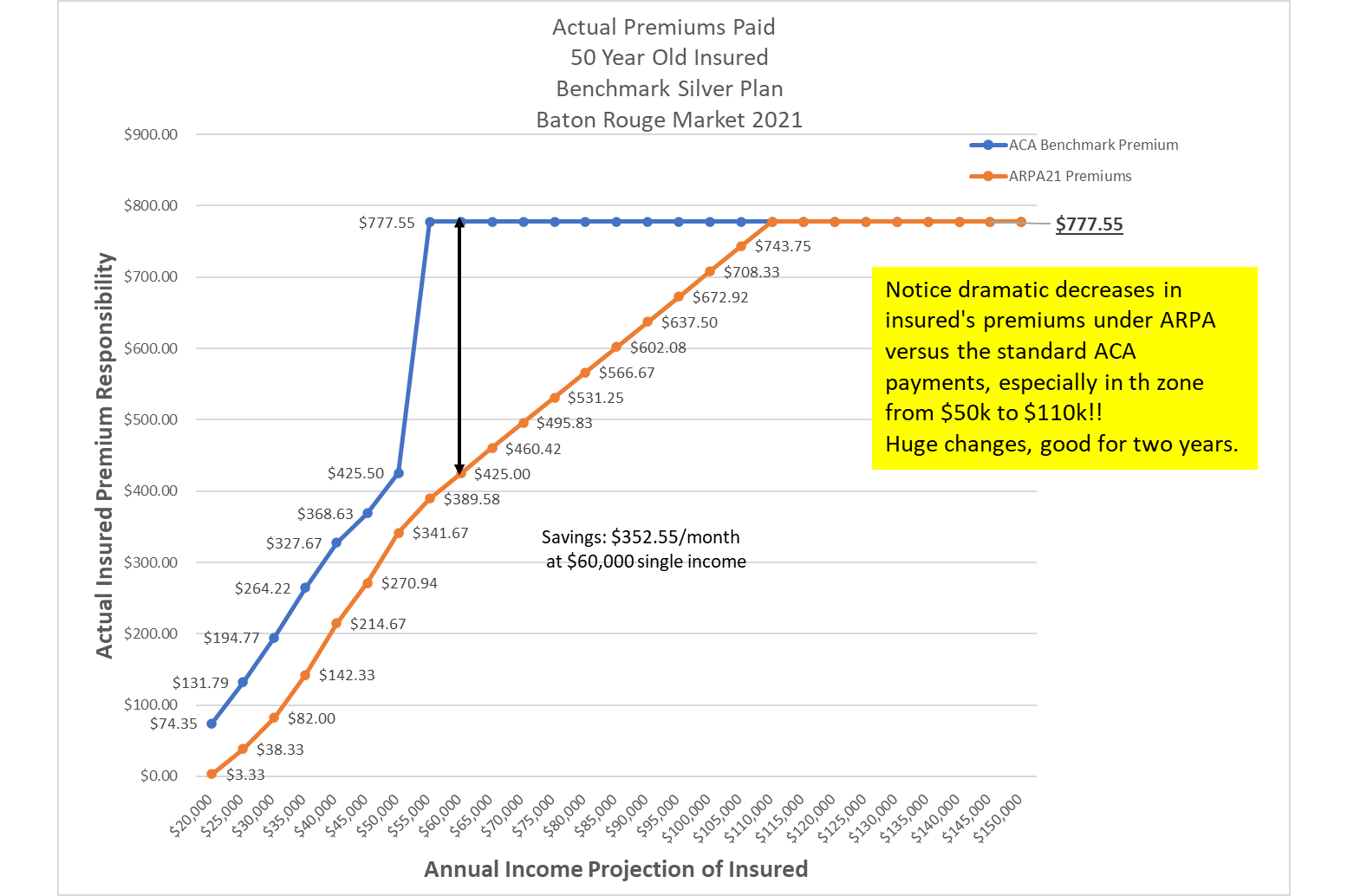

Under the ACA, prices for coverage go up with age. Likewise, tax credits go up as premiums go up. So, what do you think happens when we run these same numbers for a 50-year-old buying the same plan?

Now, we can see that under the new scheme, tax credits stretch all the way to an income of $105,000 a year, for a 50-year-old single person! For families, the deals are even better! This is really starting to look like a free lunch! So, how good can it get?

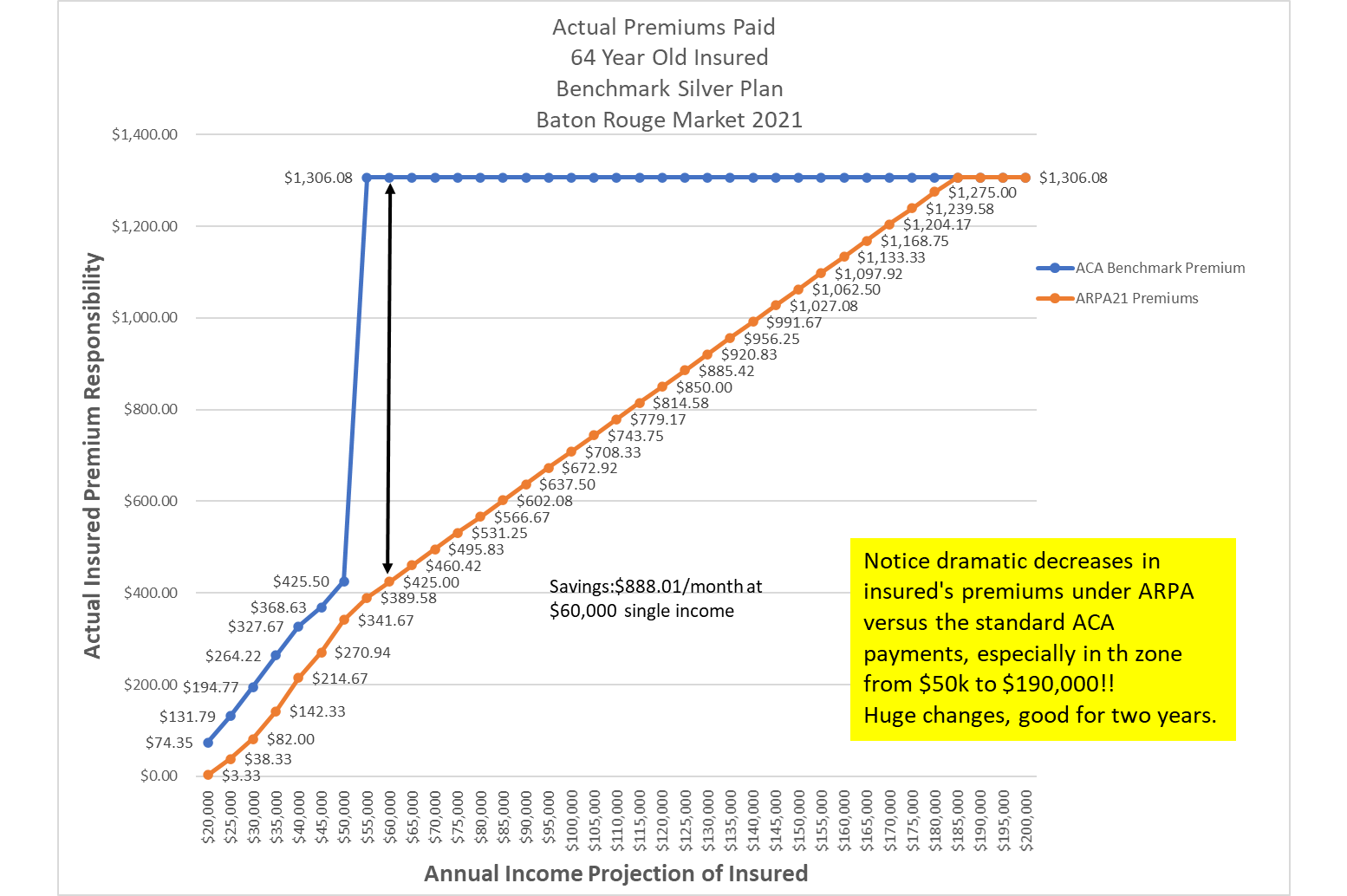

Pricing at the Margin: A 64-year-old’s new premiums:

Usually, older folks who want to retire before they reach Medicare age (65) are very, very reluctant to do so. This mainly happens because individual health insurance under the ACA rules for a 60-something is VERY expensive. In this illustration, the benchmark plan (that’s the second-cheapest silver plan) for a 64-year-old runs $1,306.08 per month!

Under the original ACA tax credits schedule, if that 64-year-old was making more than $50,000 per year, she had to pay 100% of that $1,306.08 a month right out of her pocket! That fact alone kept a lot of people in their 60s working, so they could keep their health insurance from their jobs. Kind of sad, really.

No more. Under the ARPA 21 ATCs schedule, a 64-year-old making $50,000 per year can get that $1,306.08 insurance for just $425 a month! How’s that for “too good to be true”?

But it is. Check out this grid, comparing the ACA prices to the ARPA 21 prices for a 64-year-old:

This new model is SO generous that our 64-year-old can get federal assistance to help her pay for her individual healthcare insurance even if her income is over $170,000 a year as a single! It’s not quite a free lunch, but man!

A few caveats, a.k.a. the fine print:

If you currently have a healthcare.gov plan, you have to go back to the site and re-enroll in a plan (even if you stay on the same plan) to claim the larger subsidy. The law only gives the subsidy to those who enroll after April 1, 2021. But because this is a special open enrollment period, you can do this without penalty.

If you are working and your employer offers you a bona fide health insurance plan, you are not eligible for ANY of this assistance, nor are your dependents or spouse if your employer offers them coverage, too.

These benefits are available in Louisiana ONLY if you purchase a policy on healthcare.gov. Many licensed agents and brokers do business on healthcare.gov, including our own here at Blue Cross. BUT if you purchase a plan off-exchange (meaning not on healthcare.gov) it is NOT eligible for ANY federal assistance, no tax credits at all. It MUST be a healthcare.gov on-exchange plan.

Ready to start shopping?

It’s so simple. Call 1-844-GET-BLUE. OR go to www.GetPlanOptions.com. Or, check out this easy video guide to estimate your new subsidy. Any of these can get you to the new money and the new coverage.

Straight Talk is, this is all new. It’s real. And there is no scary fine print!

Unfortunately, if you do re-enroll in the same plan to take advantage of the tax credit increase, all your previous claims do not count towards the reselected plan. Blue Cross confirmed this with me, so it’s only advisable if you haven’t really used your plan that much. If you have met, or are close, to already meeting your deductible, I would advise against it.

Derek!

Thanks for reading! At this point, no decisions have been made on accumulators. The best course for someone close to their deductible is to explore options, but not to act yet. We will keep you updated as soon as we have a clear answer.

Cheers!… mrb

See question 20. Does this only apply to Montana even though it relates to the Federal Marketplace?

https://csimt.gov/wp-content/uploads/American-Rescue-Plan-SEP-FAQ-March-2021.pdf

Mark!

Great question. When we talk about re-affirming or changing a plan on healthcare.gov during this gigantic open enrollment period (runs til 8/15 at least) the first question I get from clients and agents is about accumulators (deductibles, copays, coinsurance) for the year to date. The federal documents say no carrier is under any obligation to carry over accumulators from one plan (let alone one company) to another. Thus it’s basically “dealer’s choice” based on the carrier you are with and the one your are moving to if you are moving.

I would ask the carriers directly before you make any moves, if you’ve accumulated significant healthcare spending in your out-of-pocket buckets during 2021 and find out if they will move that credit over for you.

It’s a carrier by carrier decision. Healthcare.gov anticipates that carriers WON’T move the money, but we are finding more carriers willing to do so now.

Cheers!…mrb

What about if you pick the same plan you were in? We’ve already hit our deductible, so I’m scared to rock the boat at all. When I called BCBS, the rep was hesitant to tell me anything concrete. One of my concerns is that if I did update my marketplace app and tried to select the same plan, the pre-subsidy premium amount changes because I’ve had a birthday since I applied in December. I don’t want the fact that the premium is different to trigger it being classified as a new plan. How can I keep the same plan (with the amounts paid towards deductible), but receive the increased subsidy amount? Thanks

Again all looks great BUT NOTHING IS FREE

Who do you think all those BILLIONS of dollars are coming from? Also who and how do you think it will be paid back. You can do anything if you have an endless budget and not have to be accountable for it or God forbid have a BALANCED budget.

What would it look like if you could ONLY spend the money in you bank acct. ? I appreciate how much the new premiums help people but your opinion is very utopia. Great place to live but it’s not reality because someone has to pay for it even if it’s CHINA or our great great great grandchildren. Please explain where the money being given away comes from.

If my opinion is way off I’d appreciate your reply

Dorothy!

What a great comment! Every thought you have in your mind is currently rattling around in my mind as well. I absolutely worry constantly about the amount of debt the US is accumulating (over $30 Trillion currently, an unimaginable sum!) and how we would ever pay it back! It is scary! Here are the things that set my mind to rest on these issues, hopefully they will help you cope a bit as well.

First, it’s important to understand that the US government has a global “credit rating” just like you and I have one, that is based on the world’s perceptions of how much money our economy can create and how much our nation is “worth”. That credit rating is reflected in a very useful measure which is the interest rate the global credit markets demand we pay on a 10 year Treasury note. As long as that interest rate stays low, then some very smart people all over the world are saying that our economy can handle the debt without slowing down our growth. It’s sort of like when you go house hunting, they bank will “pre-approve” you for a certain sized house or money you can borrow.

The world does that to us every day. Check the current interest rate on 10 year Treasury notes (which we have to pay). You can see it 24 x 7 right here: https://www.wsj.com/. That number was 0.8% in November which is an historic low. With Covid and all the borrowing we are doing, we have driven that number to 1.65%, which is still really good, but not as good.

Economists like me will start to push the panic button (stop new borrowing!) when it hits 2.25%. And believe me, we are watching it very closely. Now, if I could just get regular folks getting $1,400 checks in the mail and enhanced unemployment to see and understand this!

Thanks for hanging in! Cheers!…mrb