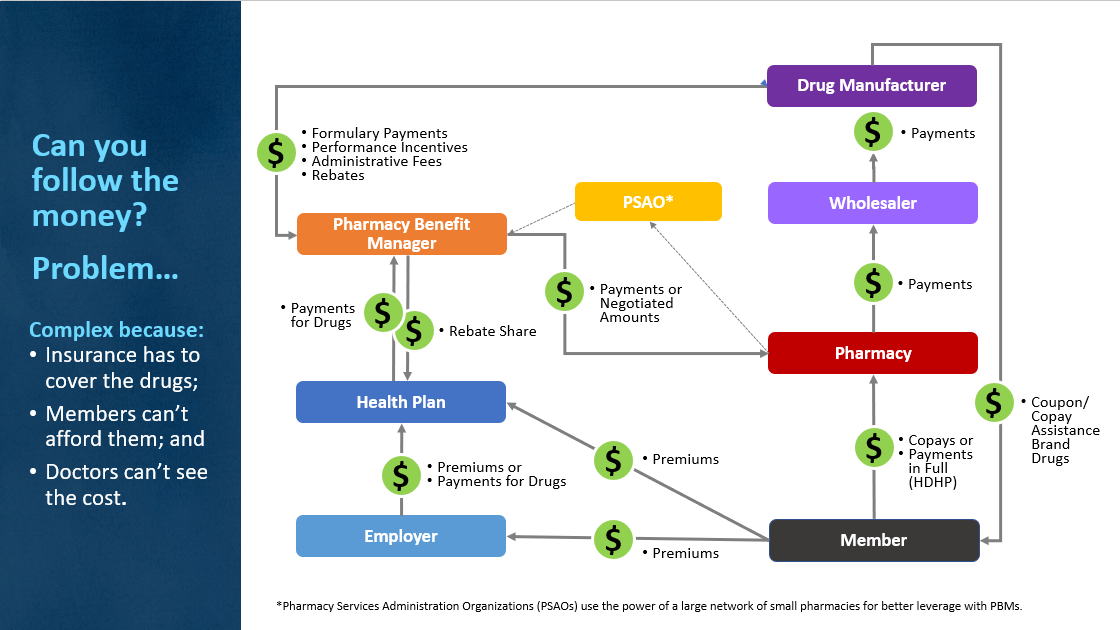

From our last discussion on why prescription drugs cost so much, you might remember we introduced this graph:

And we talked in some detail about the players we EXPECTED to see in any transaction involving prescription drugs, namely the guys on the right in the picture above: manufacturer, wholesaler, pharmacy, member/patient. These are the people in the drug pipeline who actually TOUCH the drugs themselves.

But we also pointed out that the member is often prescribed drugs that he can’t afford, or simply is unwilling to pay for. How many times have you asked at the doctor’s office how much a drug will cost you at the pharmacy? And even if a doctor wants to help keep costs down for her patients, there are so many drugs, manufacturers and health plans, she probably can’t keep up with the price structures.

But Mike, what about the guys on the left? Pharmacy benefit managers, health plans, employers; WHY do we need them?

This is an EXCELLENT question, worthy of a big-time Straight Talk Piece like this one. Let’s start at the bottom (those on the left of the chart) and work our way up.

Employers are involved because they provide healthcare insurance coverage for their employees, often picking up 80% or MORE of the tab for that coverage. Around 90% of Blue Cross members have health insurance because they have a job or are related to someone who has a job. Employers get something like $250 billion a year in tax breaks to keep their employees covered. Employers are HUGE players in covering and paying for drugs.

Health plans are involved for a variety of reasons, the main ones being that drug coverage is REQUIRED as one of the federally ordered 10 essential health benefits on your health insurance plan. In Canada, a country where drug coverage is NOT included in health plans, prescription drugs are significantly cheaper to purchase (but even they think prices are too high).

In the United States today, it is almost impossible to sell health insurance without comprehensive drug coverage. And for a health plan, providing this “expected” drug coverage is very, very difficult and expensive.

In fact, just to build a simple drug coverage plan for a regular, run-of-the mill health insurance product, Blue Cross has to pay for drugs from almost 1,200 manufacturers!

Yep, almost 1,200* of them. Just to build a simple health plan.

Starting in 2010 with the passage of the Affordable Care Act, the money insurance companies use for creating health plans, negotiating contracts and running their businesses was severely limited. In fact, as premiums come in from employers and members, we are required to guarantee that either 85% or 80% (depending on the size of the company) of those premiums are spent to pay for healthcare ONLY. Nothing else.

The 15 or 20% that remains does NOT leave enough money in overhead for us to negotiate and manage 1,200 separate vendor contracts for drugs to build a health insurance product with. Can’t be done. So how do insurance companies like Blue Cross respond to this restriction?

We hire companies who’ve already done all that work and have strong, negotiated contracts with drug companies that we can purchase within. We seek scale in contracting. These purchasing companies are called pharmacy benefit managers (PBMs).

These entities purchased almost $1 TRILLION of prescription drugs globally in 2018.

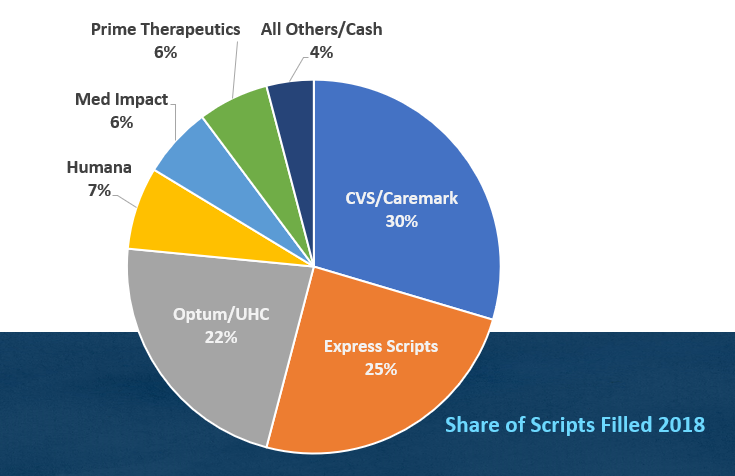

PBMs are not like drug manufacturers. There are currently only a handful of PBMs, as shown above, that control almost all drug purchasing planet-wide. In the U.S., PBMs filled more than 98% of all prescriptions written. You can see, PBMs can be huge. Our preferred PBM negotiates $280 BILLION in drugs every year on behalf of its customers like us. We only pay for $879 million a year in drugs to cover all our members. So, using a PBM gives us “instant scale” in negotiations with drug companies. We know from our own business that scale is a good thing.

That’s why you see so many lines of money running in and out of the “pharmacy benefit manager” box in the first diagram.

PBMs have size, powerful data tools, and contract relationships that save us an average of $345 per member enrolled per year here at Blue Cross. We have over one million members. That’s hundreds of millions in savings our members don’t have to pay. That’s the good news.

Mike, that makes sense. Now give me the bad news.

The bad news is these PBMs have scaled up to be so large, and have so much purchasing power that their business models can be quite complicated and opaque. Here’s a quick example of that:

Did you ever notice when you go to the grocery store soda aisle that one or two companies seem to dominate that space? Ever wonder why that is? It’s because those soda companies PAY the grocery store for the shelf space. The grocery store has a revenue item that is simply renting space on the shelves, and the space goes to the highest bidder. And they do it for chips and other products too.

PBMs do the same thing, only with prescription drugs. They sell top placement on their formularies (lists of covered drugs built for insurance companies and large employers) to the drug manufacturers who pay the most for that preferred placement. That payment is typically through rebates on the drugs as they move through the system. This means the drug your employer or insurance company recommends as the best deal under your insurance typically bought its spot on the PBM’s covered drug list. And how that’s negotiated, and how they get paid, is not public knowledge. It’s a real mystery.

Also, about half of the PBMs’ profits come from a feature called “spread pricing.” It turns out that PBMs can keep the difference between what a health plan pays the PBM and what the PBM pays a pharmacy to fill a drug for a member.

Imagine I’m a diabetic filling insulin A on my drug plan, which my insurance company pays their PBM $1,000 a month to fill. Now imagine the PBM is only paying the PHARMACY $800 for that same prescription. The PBM gets to pocket the $200 difference, that is called a “spread.” Spread pricing now makes up 50% of all PBM profits nationwide and the practice is growing.

So, Mike, as a healthcare consumer, are PBMs good for me, or bad?

The answer is, “Yes.”

It’s clear that if insurance companies had to build their own formularies, negotiate their own drug contracts, distribute and process their own drug data, that health insurance would be a LOT more expensive than it is today.

Simply put, the only way health insurance companies can meet the expectations of government officials and their customers, within all the financial restrictions imposed by the ACA, is by using a vendor who has already done all that work. I can’t see any other way under the current rules. So PBMs are an essential part of providing compliant drug coverage.

It’s also clear that the effect of PBMs’ business practices on the prices of prescription drugs are murky at best, but probably overall enable the system we already have. One where drug manufacturers can take advantage of what they believe are deep-pocketed purchasers of drugs (like governments, employers and insurance companies) to charge exorbitant prices for their products. PBMs, in that respect, are part of the problem too.

Straight Talk is we’ve gone full circle on the toughest question – “why are prescription drugs so expensive” – and we’re right back where we started:

- Entities like governments, employers and insurance companies are REQUIRED to pay for drugs in their health plans for their employees and members and are expected to have infinite resources to do so.

- Those members are sometimes prescribed drugs they are either unwilling or unable to pay for.

- Legislators have been sensitive to their pleas of unaffordability, making the coverage of certain drugs a matter of politics, instead of science.

- Physicians want their patients to have the latest, greatest drugs available and are not typically aware of costs.

- Bringing the average new drug to market costs between $2.5 and $3.0 billion.

- Drug manufacturers are excellent and lavish marketers, spending billions to build demand for their most expensive products.

- The complicated process of paying for drugs has significant numbers of middlemen involved, and the processes are opaque, making a straightforward fix for drug prices almost impossible.

- There is an expectation in the media and marketplace that insurance carriers, employers, and government agencies will spend whatever it takes to save a patient’s life. No limits.

These are the realities we are dealing with in providing drug benefits for you. And stand by, things are about to get a LOT worse.

More Straight Talk is many new drugs that treat conditions otherwise incurable and fatal are about to hit the marketplace, and the prices are expected to be $1 million and more. We’re excited about these advancements, but the question that remains is how will we manage these new costs and what behaviors will they influence? At the risk of oversimplifying it – in order to save a baby with a rare form of muscular dystrophy, we will have to ask some folks to change their heartburn medicine to lower-cost options.

My insurance doesn’t allow me to get the manufacture’s discount anymore for asthma medicine.

If companies (insurance companies included) would switch to “pass through” PBMs, the administrative cost to the sponsor would go up (a negative), but the spread pricing that makes up over 50% of the PBM’s profit would be cut out of the picture. Eliminating rebates would also promote a downward pressure of drug prices from the manufacturers, with incentive to provide the lowest price in order to capture market share and allow capitalist pressure to lower costs. The system in place promotes more expensive drugs with bigger rebates to be picked for formularies, thereby giving higher profits to PBMs, but also sustaining a high cost system that is paid for by patients, the businesses subsidizing the insurance for their employees, and massive amounts of taxpayer money through the costs of Medicare and Medicaid Part D, along with the ACA.

A perverse increase to increase prices. How long can we let this go on? I’m thinking its way overdue to get the federal government to get this system to change, and get our medical costs down from 18% of GNP to 10-13 percent of GNP like the other developed governments.

Of course, stopping the vertical monopolies that the big PBMs are forming would do alot to prevent the opaqueness of their system which enables these excess profits to be “hidden”

Chris!

If your thought is, why can’t we go back to a world without pharmacy benefit managers, rebates, and spread-pricing, here are a few obstacles you would have to overcome:

1. Size/Volume–BCBSLA is arguably the biggest insurance company with the most membership in Louisiana, and we buy over $900m a year in prescription drugs. Surely that’s enough to get us some aggressive discounts without using a PBM, right? Sorry, no. The US drug market is a highly fractured, $900 BILLION a year industry, divided up amongst 2,000 separate drug manufacturing companies. It takes 1,200 different drug companies just to build the standard BCBSLA formulary that our corporate clients expect us to have. With hard, federal caps on our gross margins, we could never hire enough people to develop and manage those relationships efficiently at our size. Without the PBM to do that for us, drug prices would go UP, not down. We even know how much, think of premiums going up $350 per person per year over 1.1 million members, and you’re starting to get the idea.

2. Scale: For all intents and purposes, there is no “cash” drug market any more. 98% of all prescriptions filled in the US last year were filled via a PBM relationship with a pharmacy. You cannot “go back” unless you want to get more government involvement which has never, as far as I know, led to any decrease in the price of anything, ever.

So while I share your nostalgia for a time with simpler relationships, customer expectations of drug coverage combined with the fractured nature of the drug manufacturing business renders this impossible. PBM’s exist because they have mastered contracting and distribution, much the way WalMart did 30 years ago. And PBM’s do it without taking possession of the product! In the current economic/legal environment, I do not expect things to change very much.

Thanks for playing!…mrb