When you research the pharmaceutical business and why drugs make up such a large percentage of our healthcare spending nowadays, you’d better be ready for a few surprises.

For example, in our first “Tough Questions” post, I was floored to find out there are more than 2,000 companies out there manufacturing prescription drugs, and almost 1,200 of them were represented in a simple Blue Cross formulary that comes with standard health insurance.

Of course, we know a ton of stuff can go wrong with the human body, and it seems there are drugs out there for nearly every problem. And we talked a bit about why drug companies don’t do more consolidating, like we’ve seen in other industries. Today, we’re going to drill even deeper into how prescription drugs are distributed and paid for.

It ain’t exactly Wal-Mart, if you know what I mean.

This graphic shows a pretty standard type of business distribution model, one we would see for nearly everything we buy. Drugs are built and sold in bulk to wholesalers, who break them up and sell them to pharmacies by the case, and pharmacies break up the cases of drugs to sell to us by the prescription. Nothing weird or unusual going on there, right? Just follow the drugs.

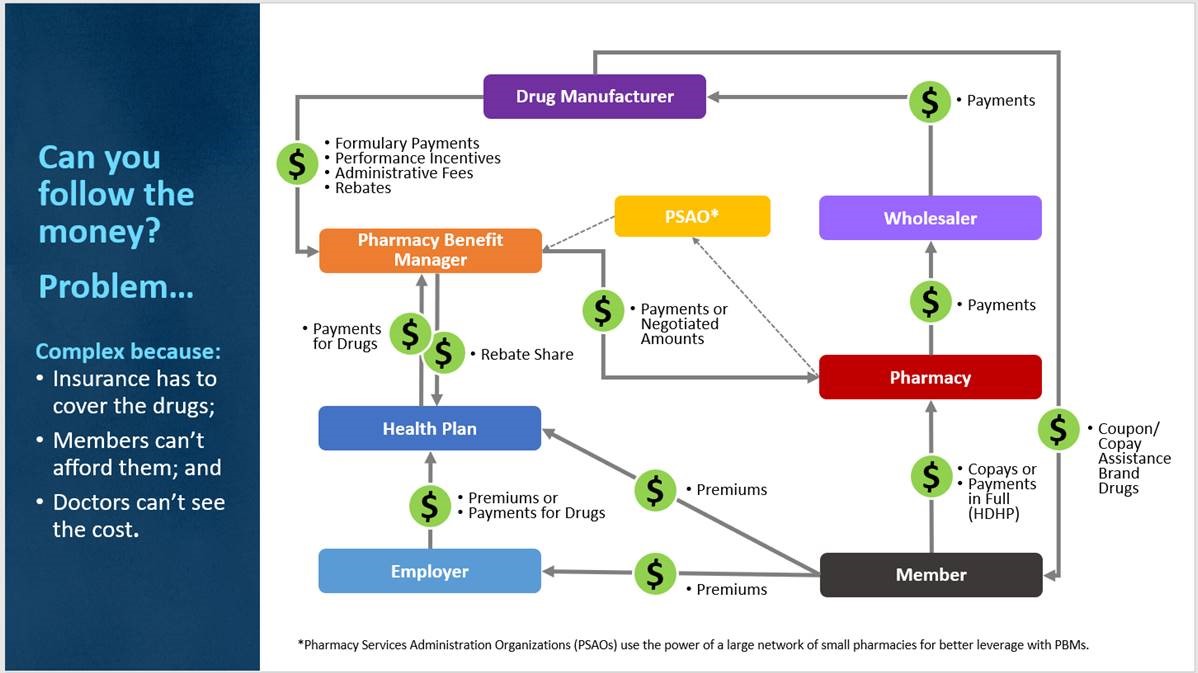

That simplicity ends when we start trying to follow the MONEY to pay for drugs. Then we get a VERY different picture, one that looks like this:

(Click to view image larger)

(Click to view image larger)If you look closely, you’ll see the same players from our earlier model, the manufacturer, wholesaler, retailer (pharmacy) and purchaser (member). And since drugs flow DOWN this diagram, you’d expect to see money flowing back up. And you do. So far so good.

But what about all this other stuff? We’ve got new players, “Pharmacy Benefit Managers,” “Health Plans” and “Employers.” Not to mention that “PSAO” box in the middle. And arrows and money going every which way. What does it all mean?

Today, let’s break down these cashflows a bit to help us understand how they build the expectations that help drive up prescription drug prices.

Who’s buying, who’s selling and who’s regulating?

You see, the “member” here has two problems in 2019. First, he’s often prescribed drugs he cannot afford to buy out of his own pocket. Second, he’s trying to protect his family from financial ruin, so he gets a job with good health insurance or he buys a policy himself, and this insurance is REQUIRED to cover a pretty hefty slate of prescription drugs (they are considered an essential benefit under the ACA).

These are problems because BOTH items add complexity to this “follow the money” problem, and complexity = cost. Every single time.

Once upon a time, back when health insurance was a LOT cheaper than it is today, insurance companies were not required to cover prescriptions at the pharmacy. Even today, the national health insurance plans in Canada mostly do not cover any drugs at the drug store. Without the purchasing power of insurance or government behind these drug customers, manufacturers know they cannot charge a lot for drugs, or nobody will buy them. So, drugs at the pharmacy in Canada are a lot cheaper than here. If they weren’t cheaper, they simply wouldn’t sell in Canada.

Here in the U.S., we have a VERY different attitude about buying drugs. Legislatively, insurance companies are REQUIRED to cover broad swaths of drugs on any ACA-compliant plan. In Medicaid plans, pharmacy coverage is technically optional under federal law, but all states currently provide coverage for outpatient prescription drugs. And for Medicare, part D drug coverage is technically optional, but 72% of enrollees have it.

Insurance companies have a very limited ability to carve out drugs that science reveals are too expensive or unnecessary because the government regulates their plans’ drug requirements. Medicaid often cannot afford the latest and greatest drugs, so they are dependent on huge rebates from the manufacturers to stay in business. Medicare plans are legally forbidden to negotiate drug prices or say “no” to a drug.

How would you like to sell in an environment where the government says deep-pocketed agencies and companies HAVE to buy what you are selling at whatever price you decide to charge them? And what would you set that price at yourself? Probably as much as you could get, I’m guessing. That’s sort of the situation we are in today.

What does this mean for me, the patient?

We’ve built a system where people who buy insurance expect that whatever drug their doctors prescribe, no matter how expensive or effective it is, will be covered, and their cost share for that drug will be small. I often receive complaints from folks about having to pay $100 a month for a drug that costs $5,000 per month. That’s not funny money; somebody is paying the entire amount on their behalf. More and more folks require maintenance medications for life, which run $50-$60,000 per year. New gene therapies are about to hit the market, and these “one-shot cures” will have price tags that run from $750,000 to $2 million plus. Whether government agencies or insurance companies or both pay these prices, everybody’s costs will be going up.

The alternative? Someone with a horrible disease would not survive, in many cases. And the crazy thing is, the drug companies designing these gene therapies spent billions getting them to work because they KNEW here in the U.S., they’d be able to charge millions and make their money back. Not so much in the rest of the world….

Increasingly, the expectation has become that everyone should have access to the most expensive drugs without paying a significant percentage of the cost. In fact, local governments often get into the act by placing hard caps on copays, guaranteeing that a manufacturer knows that an insurance company or government agency is going to foot the bill for their drugs regardless of the price, and the insured person will only be out a few hundred dollars at most. Can you see how that would encourage a manufacturer to charge a very high price for his product? Sure you can!

We followed the money; where did it go?

So, let’s recap what we’ve learned about the flow of drugs and money through the health insurance system:

- Drugs follow a simple and predictable path of Manufacturer > Wholesaler > Retailer > Purchaser

- The MONEY to pay for drugs comes from many different sources because of two basic reasons:

- Patients are often prescribed drugs they cannot (or are unwilling to) pay for; and

- Insurance plans, both government-run and private, have to buy those drugs for people with drug coverage, and they are often not allowed to negotiate pricing or say “no” to carrying a drug.

- Increasingly, expectations are that patients will be protected or shielded from the actual prices of drugs

- Manufacturers often fight any transparency legislation that would expose how much drugs actually cost to consumers.

- Local legislatures are passing more and more “copay caps” to limit how much of the cost of drugs insurers are allowed to pass on to their customers.

Next time, we’ll do some more untangling of the pharmaceutical business for you and talk about the middlemen who have evolved because of the complexity of this business. Do they actually add any value to what you are buying? Stay tuned to find out!

Here at Straight Talk, we welcome your comments and thoughts about the pharmaceutical business, how drugs and money flow through the system, and what you think should be done about that. I’m very curious how this affects our readers and would love to hear your ideas on how we can fix this.

Give it to me Straight in the comments below!

I live in a “one-horse town” (actually a two traffic light town), max 3,000 population. We have 4 pharmacies. All of the owners have a big house with a swimming pool. These are the little guys on the end of the chain and will “po mouth” about how they get beat up by everyone above them, which is probably the truth. Makes you wonder, doesn’t it?

Can you help us understand how Clawbacks work and why do they exsist? How can no-cost discount cards like good RX give me significantly lower RX prices than the Blue Cross negotiated costs? How do these discount companies make their money? Why are some folks paying Copays larger than the cost of the drug, with the extra being clawed back instead of refunded to the Customer. Why can’t pharmacists talk to us about all of this?

Kevin!

These are good and intense questions. Let me see if I can enlighten you a little upon them.

First, “discount cards” can never, ever be combined with insurance. So it’s one or the other.

Second, insurance carriers build drug coverage with over 1,000 different manufacturers on average to comply with federal and state laws about what they must cover. “Discount Card” vendors can cover some drugs, or no drugs, their call.

All pharmacy benefit manager companies, including discount card vendors, make money on “spread pricing”. You can check Straight Talk for a definition of that. You just occasionally may see smaller spreads on one vendor or the other, leading to differential pricing.

The important thing to remember is this: Your out of pocket drug spending is supposed to go towards satisfying your deductible, and your max out of pocket. If you use a “discount card” that money is gone, your insurance company has no idea you spent it and it will not count towards your deductibles and co-insurance.

It’s just a variation in spread pricing. “Discount card companies” will typically target the drugs (almost always generics) that have the biggest spread pricing at the pharmacy and try to undercut that a bit. That’s pretty much it.

thanks for playing!…mrb