Congratulations! You have managed to hang in through two parts of a rather elaborate series in which I’m trying to show what could happen if courts uphold the current court decision in Texas v U.S. declaring the Affordable Care Act (ACA) unconstitutional.

For that to happen, in my opinion, the 5th U.S. Circuit Court of Appeals in New Orleans would have to uphold the Texas v U.S. decision first, then the U.S. Supreme Court would have to do the same.

Could this happen? After 10 years of following the ACA through a raft of challenges, I don’t count any challenge out, ever. It is possible the entire law will go away. Yet the ACA has withstood some remarkable court challenges already, and we’ve basically had 10 straight years of legal battles over it. You can read all about the history of the law in my series from earlier this year, starting here.

We’ve already covered in this series how health insurance benefits could change, and how costs could change and for whom if the ACA goes away. Now, let’s talk about real-world insurance coverage and how that would change.

The Cost of Keeping Medicaid Expanded

Let’s start with the households with the lowest incomes. As I write this, more than 20 million people have health insurance coverage through Medicaid because their states “took the deal” when the ACA put expanded Medicaid on sale. The expansion covered all households below 138% of the Federal Poverty Level, which is more than half a million households in Louisiana alone. Funding this expansion requires many billions of federal dollars (more than $3 billion just in Louisiana), which would vanish if the ACA vanishes.

Suffice it to say, that’s more than 20 million Americans who could lose their health insurance virtually overnight unless Congress figured out a way to cooperate and keep that money flowing. What is clear is that most of the states cannot afford to take over those payments without federal help. You might even argue that Congress itself will struggle to fix this problem in an era where the federal government is already spending way more money than it is taking in. How much more can it handle?

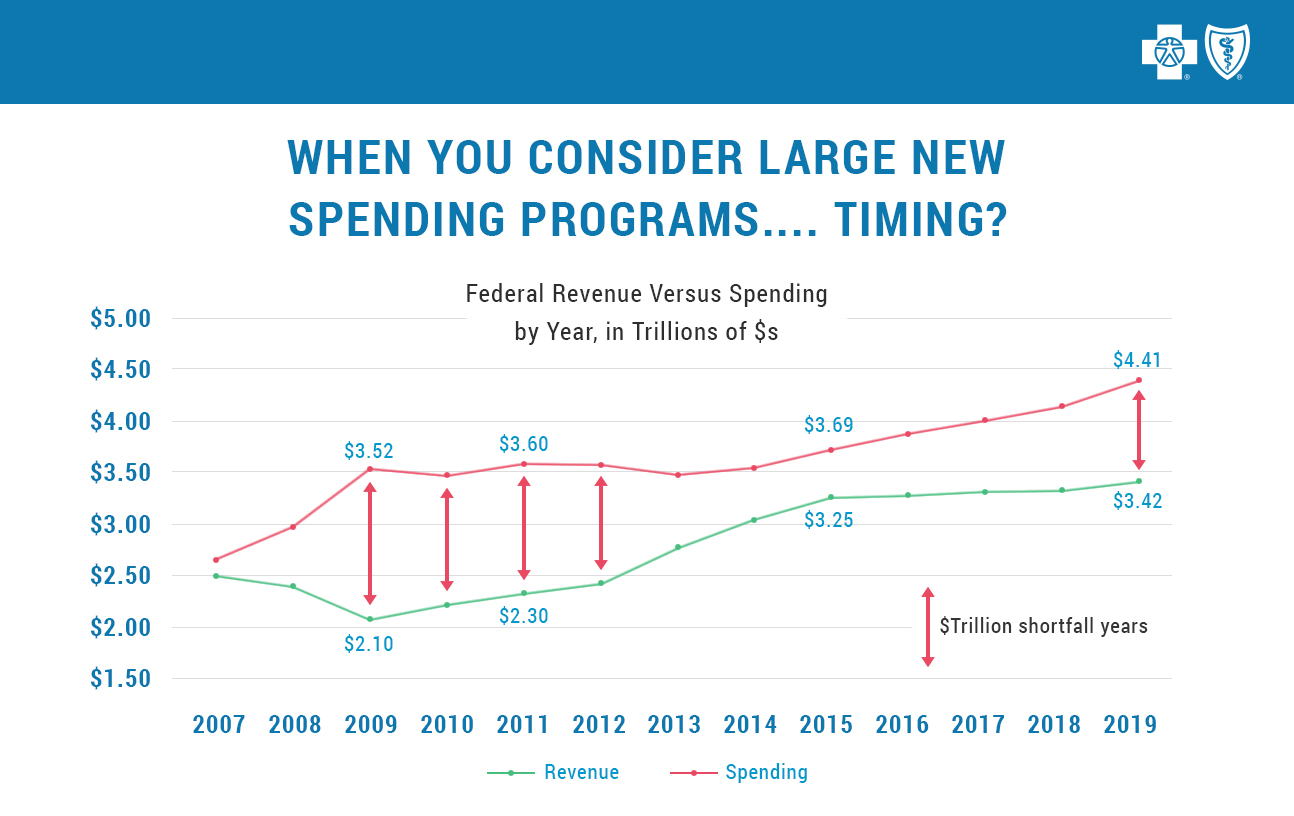

Here’s a picture for you. Note the red arrows indicate years in which Washington D.C. has spent more than $1 trillion more than it took in! Wow, what a pattern!

Around 10% of the shortfall in 2019 is strictly to cover the federal government’s payments to states for expanded Medicaid programs.

You can imagine the battles in D.C. over that. At the same time, does any judge, or panel of judges, have the stomach to strip 20 million people of their health insurance overnight, no matter how solid the case?

Seems unlikely, but what judges might do is give Congress a timeframe to fix what’s wrong with the ACA. I can’t even visualize those fireworks, so let’s wait that one out for now.

A Mess in the Marketplace

What about people who make more than 138% of the Federal Poverty Level? Around 10% of privately insured citizens get their coverage from the individual health insurance marketplace, healthcare.gov. Some states run their own marketplaces, but many, including Louisiana, use the federally run marketplace.

These marketplaces sell insurance with ACA-specified broad coverage, ACA-specified pricing formulas, and ACA-required benefits, all with an ACA-required offer to everyone regardless of their health status at the time of application.

Get the idea? The marketplaces run nationally based on ACA rules and funding. The vast majority – 90% – of the people who buy coverage through healthcare.gov get significant amounts of federal money to help them pay for their premiums and their cost sharing, like deductibles and copays. I saw a recent estimate that nearly 11 million Americans were buying coverage this way in 2019.

If Texas v U.S. is upheld? Gone.

Marketplaces created under the ACA require a lot of money to operate, around $90 billion a year. (In the graphic above, marketplace funding is about 9% of that shortfall.)

Highly valued features in the marketplace, like being able to buy coverage without being asked any health status questions or consideration of pre-existing conditions are entirely dependent on that funding. Without the ACA money, insurance sold in the marketplaces would be so expensive, very few could afford it. At least nine million of the 11 million people getting insurance through the marketplace now would be uninsured if the ACA went away, by my estimates.

Watch for Workplace Changes, Too

Well Mike, I get my insurance through work, just like 170 million other Americans. At least the ACA going away won’t affect me!

Well, everybody needs to look on the bright side …but, come on! If the ACA didn’t affect your insurance at work, why has your boss been complaining about the law for the past five years or so?

The reality is, the ACA contains a ton of rules and regulations that force employers at or above a certain size (50 full-time equivalents of labor, on average) to offer coverage to every employee who works more than 30 hours per week.

It specifies a standard for “affordability” that every employer has to hit. It specifies “essential health benefits” that your employer plan is required to cover. It requires employers to offer coverage to dependents. The ACA means employers have to cover a bunch of things like immunizations, annual check-ups and birth control at zero cost to their employees. And, it puts hard caps on the profits of the insurance company your boss is doing business with to help slow the growth of premiums.

To, if Texas v U.S. stands, employers will be free to do lots of things you might not like. They could stop offering coverage to anyone working fewer than 40 hours a week, or charge a lot more for coverage, or cover a lot less stuff on your policy, or stop offering coverage to your dependents, OR stop offering coverage to YOU! None of these things are allowed today, but without the ACA, employers would be free to do a lot of stuff they can’t do now.

It turns out, there is no part of health insurance that the ACA didn’t regulate. Even your employer, free from the ACA, could do a bunch of things that might help the business out, but might make your situation as an employee much worse.

The last estimate I saw was that the employer mandate requirement alone encouraged companies bigger than 50 full-time equivalents of labor to cover an additional 6 million people since 2015, when it went into effect. Those 6 million, and much more about employee coverage, would be at risk if the ACA went away.

So let’s see, that’s 20 million people getting covered through Medicaid, 9 million getting covered through healthcare.gov, and 6 million covered in the employer market today. That’s 35 million people losing coverage at a minimum, if Congress can’t replace the funding and rules in the ACA if it is struck down. And, the real number could be much higher. Louisiana’s share of that could hit 750,000 people or more losing the coverage they have today, by my count.

Pretty serious stuff. Definitely worth following Texas v U.S. to see the final outcome. The 5th Circuit will hear the case in July 2019, which will get the ball rolling. I’ll be watching this as it develops, to give it to you Straight.

Part 1: Your Health Insurance Benefits and Coverage

Part 2: Will My Health Insurance Costs Go Up, or Down?

Mike:

Amazing information. Scary too.

Hopefully common sense and compassion can meet in any changes in healthcare reform.

Wayne Schellhaas