When a “Bailout” Isn’t a “Bailout”:

I really enjoy Twitter. Just a few days ago, after I tweeted about a particular federal program that helps poor people pay for their health insurance, I got this response above.

Sometimes seeing the raw, unvarnished truth about how people are feeling is quite valuable. Since Twitter is global, I always assume there are more people out there who would share the same sentiments. This is America, and they are totally entitled to their opinion.

My job, on the other hand, is to shed some light on the assumptions underlying such a Tweet and give the Straight Talk on healthcare costs.

This particular Tweet was about a federal program called Cost Sharing Reductions, CSRs for short. I’ve written about CSRs before here, and explained how important these payments are to make insurance more affordable for some 100,000+ people in Louisiana, including 50,000 of our own Blue Cross customers. They are your friends and neighbors, and mine too.

Where Does CSR Funding Go?

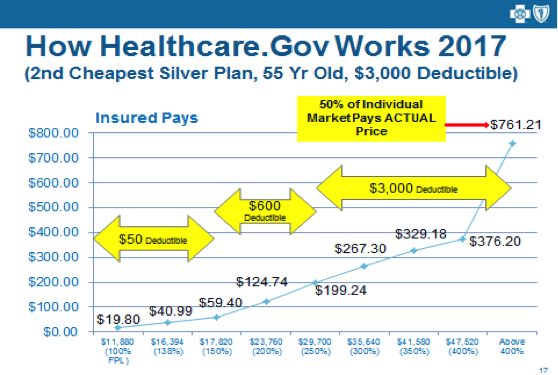

I’ll give a quick review of how CSRs help defray costs for lower-income customers. Here’s a picture that might help:

The slide above demonstrates the 2 types of federal assistance available to lower income folks on healthcare.gov

- Notice how a person’s premium contribution (the line graph) drops as their income drops.

- Notice how their cost sharing (deductibles, copays, etc.) are reduced based on their income as well (yellow arrows)

From the graph above, you can see that two streams of federal funding flow to lower-income folks who buy Silver plans on healthcare.gov for their individual health insurance needs: Advanced Tax Credits and CSRs.

Advanced Tax Credits subsidies are responsible for lowering the premiums from the base $761.21 per month to as low as $40.99 per month if a person’s income drops to about $16,400 a year as a single. People whose incomes fall lower than that would typically be eligible for Medicaid.

But, the complaint in the Tweet above, and what I’m addressing today, is about CSR subsidies that go directly to lower out-of-pocket costs (like copays and deductibles) for lower-income folks.

Notice this Silver Plan has (by federal design standards) a $3,000 deductible and a maximum out-of-pocket cost of almost $6,000 per year. On the lower-income part of this scale, we are talking about people making maybe $18,000 a year. What are the odds they will ever raise the money to cover a $3,000 deductible? Pretty slim. You can imagine that without the CSRs taking their deductibles down to as low as $50 a year, lower-income folks with private insurance would hardly ever use it.

That’s why the federal government included CSR subsidies in the plan designs under the Affordable Care Act (ACA) – to make health insurance more affordable for them, and to provide funding for insurers to offer CSRs in plan designs for eligible customers.

How Do Insurance Companies Use CSR Payments?

But, my irritated Twitter friend above does raise a valid point: Why do insurance companies need more money from the government to pay for care for these folks? Is it really a “bailout” to very profitable companies?

I can’t speak for every health insurance company in America, but I can tell your from the perspective of Blue Cross and Blue Shield of Louisiana, “profits” from healthcare.gov business have been pretty hard to come by the past few years — we’ve lost more than $200 million since 2014.

And, the fundamental design of how these CSRs actually work shows they are not a bailout for insurance companies. You see, a CSR payment from the federal government is essentially a pass-through.

An insurance company like Blue Cross can only use that money to pay the cost-sharing for things like copays and deductibles that real members use for real treatment.

In fact, every quarter, the federal government reconciles the CSR amount it sends to an insurance company with the amount that company’s eligible customers actually used. If there’s a difference, the federal government can take back any unused funds or move them on to the next person who needs it.

By law, insurance carriers cannot make one cent of profit from a CSR payment. Not one cent.

Does that sound like a “bailout” to you? Of course not.

So, the Straight Talk is, CSRs are a direct subsidy to the working poor that pass-through insurance companies to help make their coverage more affordable. Carriers may not profit from this pass-through, and federal audits guarantee that fact. Period.

Why The CSRs Are Such a Hot Topic

One other important point about CSRs: while the ACA is still the law of the land, Blue Cross and other insurers selling plans on healthcare.gov are legally bound to offer CSRs to eligible customers. In the event the government doesn’t fund them, we must absorb the higher costs and factor in those costs when setting premium prices.

That uncertainty is what’s driving a lot of the 2018 premium rate increases we’re seeing reported in the news these days. Here at Blue Cross, if there had been guaranteed CSR funding, we would have had a single-digit rate increase on average for 2018 plans, instead of filing a double-digit average rate increase.

That’s the Straight Talk: No “insurance company bail-outs” here.

Good commentary. I appreciate knowing how it really works as opposed to the here say about how people think it works.

Ok but my problem with Insurance companies – and I’m all for insurance companies making a profit (it’s the American way) – you never give back money. So lets say for 2016 you raised premiums, but the Feds gave you the subsidy – so why are you raising rates again in 2017? Then the whole – we don’t make a profit – so we have to raise premiums and cut providers. Let me see – how much is your foundation????? Last time I read an article about it – it was something like over $300,000,000. My understanding is you roll your profits into this fund and then claim you didn’t make a profit, but yet you are sitting on a gold mine of money. This is my problem with Blue Cross.

why do insurance companies create pools of insureds? I thought everyone as a collective group covered the cost. I think we should return to the founding thesis of insurance. Now days our insurance cards are being used as if they were bank cards.

This is an excellent, although wonky, question. Insurance companies group clients into pools of similar types of business, or at the direction of the federal government.

For example, individual health insurance purchasers and group purchasers are required to be separated financially by federal law so that we can report how much of their premiums were spent on healthcare SEPARATELY. The individual clients have to have 100% assurance that at least 80% of their premiums bought healthcare, and the groups 85%. Carriers aren’t allowed to cross-subsidize the pools when setting rates.

This is one of many “sortings” of the insured population required by federal and state law.

The good news is, BCBSLA last year spent 85% of all premiums on healthcare across the board, and another 4% of premiums were paid in taxes and fees that ultimately bought healthcare for other people, either via the Medicaid Expansion, or Advanced Tax Credits and Cost Sharing Reductions paid on exchanges. Almost 90% of premiums bought healthcare.

Thanks for the question!!…mrb

Kim!

Thanks so much for sharing your feelings about this issue with us. As a member of BCBSLA we want to make sure you get all the transparency and information we have about where your money goes, and how it is spent. Hopefully this will help answer your questions.

The money we are referring to in the article above is not a subsidy. It is money that the Fed gives BCBSLA in trust to send to doctors, hospitals, and other medical providers directly to cover the deductibles for very low income patients. It’s not our money, and if it wasn’t there, the money would come out of the members pocket as their deductible. It has nothing to do with our costs at all, and thus, does not affect premiums UNLESS it is cut off and we are required to replace it. Which blessedly has not happened yet. We will only raise rates to cover those costs IF the Fed cuts off the funds, which they have threatened to do but not done yet.

Every insurance company, including us, is required to give you, as a member, a rebate on your premiums if we can’t demonstrate that a very high percentage of your paid premiums does not pay directly for someone’s medical care. Last year, 85% of all the money we got in premiums went back into medical care for our members like you. Another 4% paid the taxes that bought the medicaid expansion and actual subsidies on healthcare.gov. If we ever fail to do this, and we make a profit because of it, you will be entitled to a rebate.

Finally, the BCBSLA Foundation is an important community support organization whose annual budget is less than 1% of the number you quoted above. As a member you are entitled to this information, but the number you quoted above is nowhere near reality, I can assure you. I’m sorry someone has given you such a dramatic misrepresentation of our Foundation. They do a lot of good in the state with much, much less money than you quoted.

We annually reconfirm our commitment to staying in the unstable individual market and trying to fix it as a part of our commitment to Louisiana. As a not-for-profit company whose mission is to ‘Improve the Health and Lives of Louisianans” we take the obligation of serving the individual market and trying to fix it. We have invested over $200M in real losses to support Louisiana’s individual market, and we will continue to do so because over 100,000 of our friends and neighbors are counting on us.

Thanks again for reaching out! Please let us know if we can help in any way.

mrb

Mike keep stating the facts. Always a pleasure listening to your presentations or reading your articles. You are man of the numbers and numbers don’t lie.

Very good indepth explanation of the way the ACA works

Thanks Mike ,

Your answers were “spot on” … Thanks you for making it clear about

the non-profit status and the facts that support the truth.

Warmest Regards , Harold Smith … Houma La.