One dear love in my life is what my wife calls my “tractor time.” Our house sits on about an acre of land, which creates quite a few mowing opportunities during the year. Each year, I mow the full lawn around 25 times at about an hour each.

In 2008, I purchased a brand new big green lawn tractor to help me with this chore. If memory serves, I paid around $1,800 for it. Since that time, it has served me very well, mowing that acre over 200 times! This spring when I pulled it out, there were some maintenance and repair issues that surfaced, and so I was faced with some interesting decisions.

The repair/replace needs were extensive (it is 14-years-old, after all) and me being me, I began to work through the costs and weigh out my options. During that work, I realized that over time, my tractor and I had saved us over $13,000 worth of paid yard work! That was my NET savings, after the cost of buying the tractor, maintaining it and putting gas in it. New equivalent machines are running about $2,500 nowadays, but I got the old one back in fighting shape for about half that much.

I just took it for a spin about five minutes ago and it cuts like new! Money well spent. Doing that math, and then spending an hour on my running-like-it’s-brand-new tractor got me thinking about some much larger investments and value that we all seek. You know, I do a lot of thinking on that tractor.

What value do you get from your health plan?

I’m betting most of you are putting money into your health insurance every month. Including what you pay, plus any contributions from your employer or the federal government, it’s probably a LOT of money. So, what’s the value?

It was easy for me to compute the value of my tractor for me and my future mowing needs. Can you do the same calculation for the protection your health insurance is offering to you and can you tell overall if it is giving you a good deal?

I can help you answer that question.

I often tell folks that a serious function of our operations here at Blue Cross is to daily provide Louisianians with health care they could NEVER afford to pay for on their own. A serious part of that conversation (the Straight Talk part) is when we discuss transparency and how Blue Cross spends your money. I like to update you on where your money went so you can see the value of your investment in us. To honor that commitment today, here is our Dollar Bill Income Statement for the calendar year 2021:

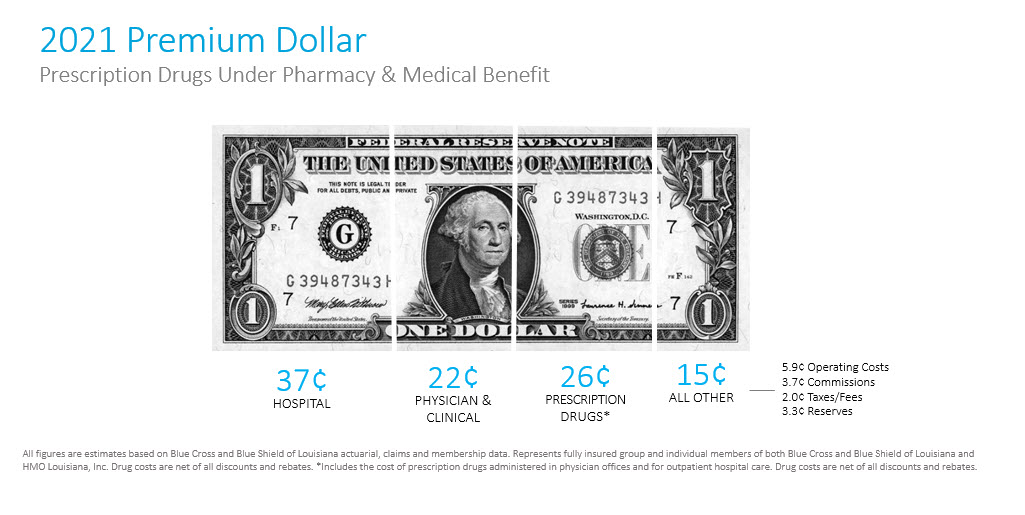

Breaking down the dollar

From the diagram, here are some important numbers to take with you.

First, the money coming in from all of our fully insured members during 2021 was $3.8 billion! I am always so humbled when I realize that the good people, businesses, school boards, government agencies and the like here in Louisiana trust us with such an enormous sum of money and have continually trusted us since 1934. But the important question is: during 2021, where did all that money go?

The largest slice of the premium dollar went to pay directly for Blue Cross members’ inpatient hospital bills. Those bills alone consumed 37% of all the money that came into our company. That’s about $1.4 billion we paid to hospitals in 2021 on behalf of our customers.

The next largest slice was the cost of medications/prescription drugs for our members. These drugs are purchased in hospitals, at doctor’s offices and clinics, AND at the pharmacy. Getting everyone their meds during 2021 consumed 26% of our total spend, or roughly $988 million! That means we bought almost $1 billion in medications for our members in a single year. And that’s a slightly LOWER percentage of our spending in 2021 than it was in 2020. So yep, 37% of the money we took in went to hospitals and 26% went to drugs.

Notice we’re already up to 63% of your money spent, and we haven’t even paid a doctor bill yet!

Our payments to doctors, clinics, labs and other outpatient settings totaled 22% of the premium dollar in 2021. Think about all the things your doctor might order for you in an outpatient setting and you’ll start to understand this category of spending. That 22% of the total means about $836 million was spent on this category alone, where your doctors get paid along with providers and services they order for you.

So, we’ve already accounted for 85% of the total amount of money Louisiana’s people, businesses and governments have invested in us, and we haven’t paid a nickel of Blue Cross salaries yet.

Like everyone else, we’ve got taxes and usage fees to pay to stay in business. Those taxes and fees consumed another 2% of our premiums, which is roughly $76 million. So now we’ve accounted for 87% of inbound premiums.

Paying the independent brokers and agents who work with the 90% of our customers getting their insurance through a job took right at 3.7% of the total premiums paid in 2021. Now we’ve accounted for almost 91% of your premium dollars. Time to pay my salary yet? I don’t (usually) work for free, you know!

Yep, let’s go ahead and do that. Turns out that because of our strict expense controls, Blue Cross can serve over a million customers and nearly 20,000 businesses with health insurance each year on an operating spend of less than 6% of the total money our customers pay in through premiums. Yep, less than 6% of all the revenue we took in during 2021 paid for our operations. And that includes staffing eight regional offices around the state (Alexandria, Baton Rouge, Houma, Lafayette, Lake Charles, New Orleans, Monroe and Shreveport) and all of our core operations folks, most of whom report through our headquarters in Baton Rouge. We really do run a lean ship.

If you’ve been keeping up with the math, you’ve probably noticed we managed not to spend around 3% of all the money people paid in last year. That surplus was invested in our rainy-day fund, designed to allow us to keep paying for your health care even if we have a catastrophic interruption in our revenue or ability to operate (like we did after hurricanes Katrina or Ida).

It’s important to note where money DIDN’T go. Since we are a not-for-profit insurer and a Louisiana- based company, you never have to worry about your premium dollars ending up in the hands of some anonymous, out-of-state investor without a stake in Louisiana’s health care. Every cent of every premium dollar goes to paying for your health care, directly running our company or saving for the future.

The Straight Talk is, that’s where your premium payments went in 2021. Remember our mission, “to improve the health and lives of Louisianians.” In fulfilling that mission, we try to be extremely careful with your trust and your hard-earned treasure, because we are Blue Cross customers, too. And we appreciate each and every one of you very much.

Thanks, Mike for another clear, concise answer to a common question. Can’t tell you how many of your articles I have used to send to clients.

Mary Ann!

Thanks so much for your kind words! Remember, Straight Talk is a TEAM of people who work very hard to make our content relevant, clear, and easy to digest. Let’s thank Lindsey, Kristen, Desiree, and Nancy today!

Thanks all!…mrb

Great article, Mike! It explains why our healthcare system is so convoluted and upside down.

I admit BCBSLA is doing what it can to help alleviate this unmitigated disaster for most Americans, as long as they are working and can afford to pay the hefty premiums (or get assistance through the Affordable Care Act).

What it doesn’t show is how a Single-Payer healthcare system that every other western nation has would fix most, if not all, of this. The tax amount that is taken to pay for such a system, once spread across the entire US population, would be less than the typical premium. Plus, it would remove the requirement that an individual work where healthcare insurance is offered (or be covered due to age or income status)–they are just covered plain and simple. And Single-Payer does not mean the end of health insurance. It means that companies such as BCBSLA would have to adapt to survive (something hard for most companies like this to do, admittedly) and sell supplemental insurance. It works well for Aflac. It’s not impossible.

DJ! Sorry it took me so long to address your comments, I’ve just got my access back to comments and am catching up!

Here are three reasons why “Single Payer Healthcare” is not an option for us here in the US.

1. Our healthcare providers, already in shortage, would have to be paid significantly less than they are paid today to lower costs as you suggest. Current estimates are that we would lose 1/3rd of our medical capacity. Imagine the wait times then?

2. Over the last 20 years, government agencies (like HHS, or LDH here in Louisiana) have been outsourcing the risk for their healthcare insurance plans (Medicaid, Medicare, FEP, etc) to private health insurance companies. Almost all Medicaid members are in private plans now. Over 50% of Medicare members are in private plans. All federal employees are in private plans. AS a result, these agencies no longer have the people, skill, expertise, back office, or capacity to run a health plan. Governments have divested themselves of every function required to operate “single payer health plans” and without insurance companies would not be able to run or offer them.

3. The tax amount you mentioned is huge. In the UK, for example, where about 80% of their population uses their national health service, which pays docs and hospitals far less than we pay them here, requires a 20.5% value added tax on EVERY transaction, at wholesale AND at retail. WE’ve done the analysis many times, the only way to make SP happen is to drastically cut services and increase wait times. I doubt the average American would put up with that.

But the debate continues! Thanks for playing!…mrb