When I was young, my dad and I spent a lot of time, days even, in boats on the water. One time, when I was about 11, we were crawfishing. We had a large aluminum boat loaded with two smaller boats (pirogues) and a lot of other gear.

We found our way into flooded woods and the crawfish were everywhere, even clinging to the trees just below the waterline. Dad pointed in one direction, saying “You take your pirogue and about 25 of these drop nets and go that way. Put one out about every 10 yards or so and then come back here and we’ll start checking ‘em.”

He then gave me a long, long lecture about making sure I looked back every so often so I could find my way back to the big boat. “Nothing looks the same when you’re going out, and when you come back you won’t be able to see a thing. You’ve got to make sure you know what behind you looks like!” He just went on and on and on, until I was pretty aggravated. I yelled, “I got it, old man!” and paddled off.

By the end I was at least 300 yards away from the big boat, paddling through dense woods. When I ran out of nets, I turned around and had no idea where I was, where the big boat was or where he was. Ignoring his advice, assuming I knew better, I had zeroed in on what was in front of me, never looked back, and was truly lost.

I yelled for him, and fortunately, he yelled back. I was able to guide myself back to the big boat following the sound of his voice. I was pretty scared! You can bet I never took what I know, or what I don’t know, for granted ever again.

What You Don’t Know Can Hurt You

Some research recently hit me hard … It was about what people don’t know about their health insurance coverage! In a survey of people who mostly said they were pleased with their private health insurance, their understanding of even the most basic terminology was, shall we say, lacking.

As part of my effort to remedy that, I offer you Health Insurance 101 updated terms and financial lessons. I hope this will get rid of some of that lack of knowledge about what health insurance is, and how it works.

First, let’s review basic terms. Like every other field, insurance has its own language, which I try hard to AVOID here at Straight Talk, but you still need to be familiar with them:

- Premiums— The fixed amount you pay each month for membership in an insurance pool. You will pay this each month regardless if you get care or meet your maximum out-of-pocket costs (see below).

- Deductibles—The amount you must pay for care out of your own pocket before insurance starts to pay.

- Coinsurance—What you must cover AFTER you meet your deductible UNTIL you spend your out-of-pocket maximum.

- Max Out-Of-Pocket—The most you must pay for in-network care in a given benefit year. Once you spend this amount, your carrier will take over and pay all of your covered in-network costs at 100%.

- Copays—Fixed payment amounts for covered healthcare services.

- Networks—Medical providers who have contracted with health insurance companies to accept set amounts for services. By design, networks lower unit costs and protect patients from extra billing.

- Formulary—An approved list of drugs that your health insurance plan will cover and how they are covered.

- Claims—The invoices medical providers send to your insurance company so they can get paid.

- Rebates—Money sent back to an individual or a group when insurance companies exceed federal regulations for gross margin (that is, take in too much money).

You should probably keep this list handy until you get comfortable with all these terms.

How Does This Work in Real Life?

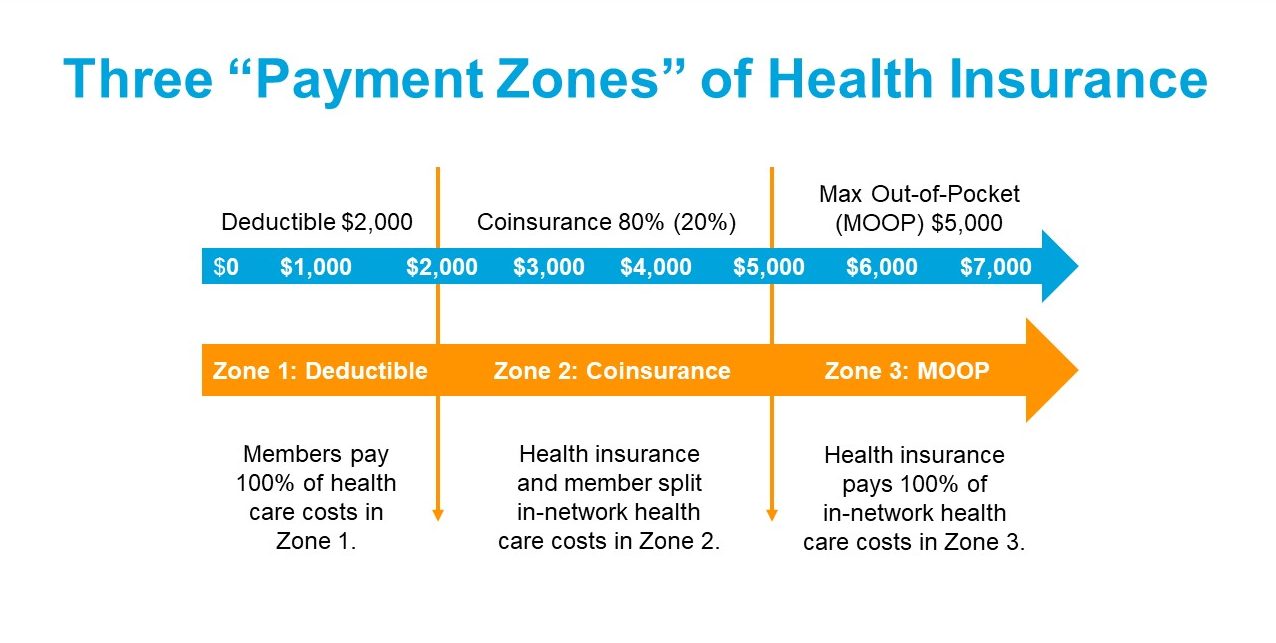

How you pay for coverage can be challenging to understand. Here are basic examples of how your payments should flow during a benefit year. For this example, let’s assume you have a health insurance plan with a $2,000 deductible, 80%/20% coinsurance, and $5,000 max out-of-pocket for in-network care.

As your health bills start to come in during a new benefit year, you and only you will pay the first $2,000 of costs. That’s your “Deductible Zone” of payments. You should know that when you are using in-network services, you are getting that care at a significant discount. Providers in your plan’s network agree to charge you below their usual billed charges.

Once you’ve spent $2,000 on in-network health care costs, you enter the “Coinsurance Zone.” Spending in this zone divides between you and your insurance company. In this example, you will pay 20% of the new charges, and the health insurance company will pay 80%.

This arrangement continues for in-network care until you have spent $5,000 total (including your $2,000 deductible spending). At that point, you enter what we call the “Max Out-of-Pocket Zone.” Your health insurance carrier will pay 100% for the care you get after that—as long as it is covered by your plan and in-network. The only thing you will keep paying is your premium each month.

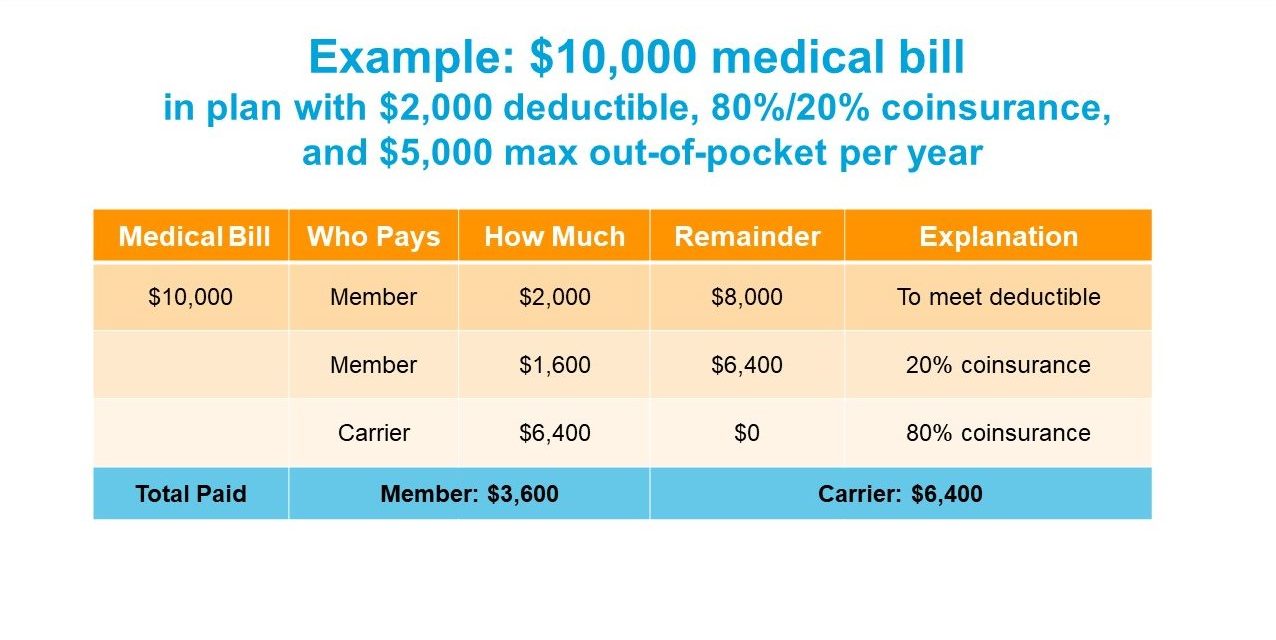

Let’s look at a couple of examples. First, a $10,000 medical bill right at the start of a new benefit year. Remember, in this example, you have a $2,000 deductible, 80%/20% coinsurance, and a $5,000 maximum out-of-pocket for in-network care.

Notice in this first example, you (the member) pay the first $2,000 of the $10,000 owed to meet your deductible. Then you split the next $8,000 with the carrier through coinsurance. You pay 20%, or $1,600, and your insurance company pays 80%, or $6,400.

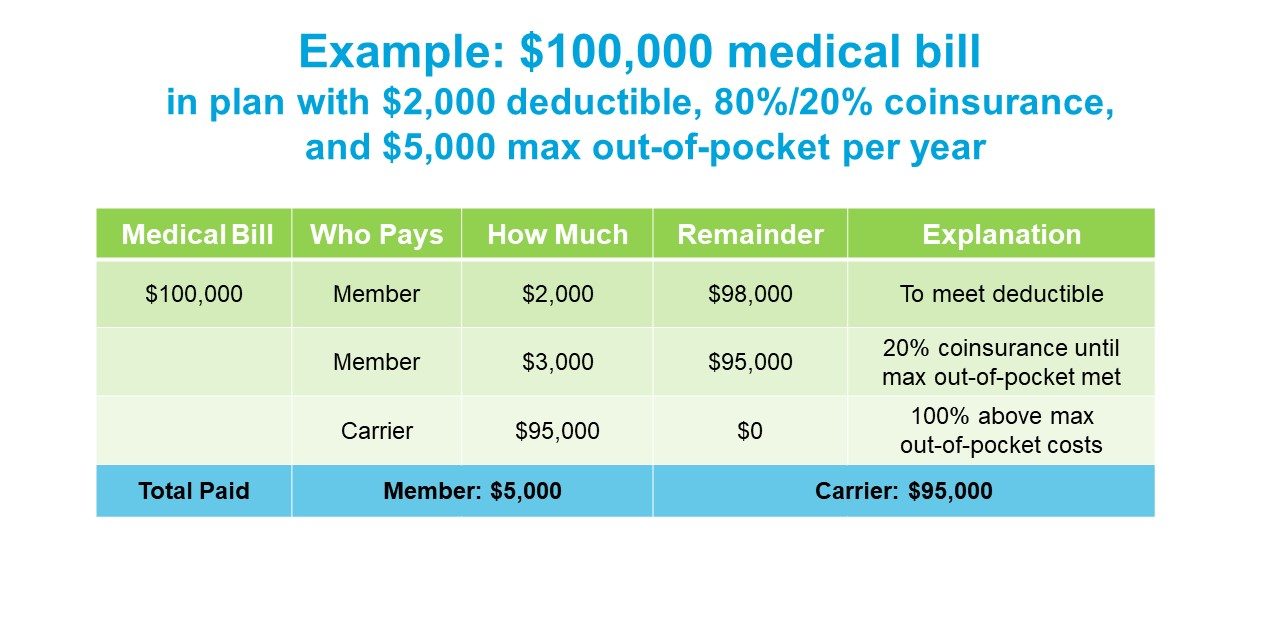

But how does this work with a much more serious accident or illness? Let’s examine a $100,000 in-network bill:

In this example, you quickly pay the entire max out-of-pocket requirement. That leaves your insurance company to cover the lion’s share of the bill ($95,000!). It’s clear when you get really sick how valuable your health insurance can be.

As before, you pay the first $2,000 to meet your deductible. Then you split the next charges 80%/20% (coinsurance) right up to the max out-of-pocket of $5,000. For the rest of this benefit year, insurance will cover 100% of in-network care for anything else you need. You can see quickly here how important it is when you access care to stay IN-NETWORK.

Even though you meet your max out-of-pocket costs, you will pay your premium each month of the plan year.

I hope these details and examples will help with basic understanding of what health insurance covers and pays. We will cover examples of plans with copays in another post soon.

The Straight Talk is, this kind of knowledge is FAR too important for me to assume everybody just knows it. The last thing I’m going to do is leave you all lost and paddling in the woods!

Thanks for the simple explanation. Will you be doing a simple explanation of how primary and secondary insurance cover costs? For example, will secondary insurance cover the 20% you pay when you are in the Coinsurance Zone?

We have added this to our list of possible topics to cover! Thanks Bobby.