I’ve always said that I can handle bad news as long as I know it’s coming. I think most people would agree with me on that one. Just don’t ambush me with bad news, and I’ll be ok.

One of the real growing concerns among our customers is a bad news ambush known as “surprise billing,” and it is mighty unpleasant.

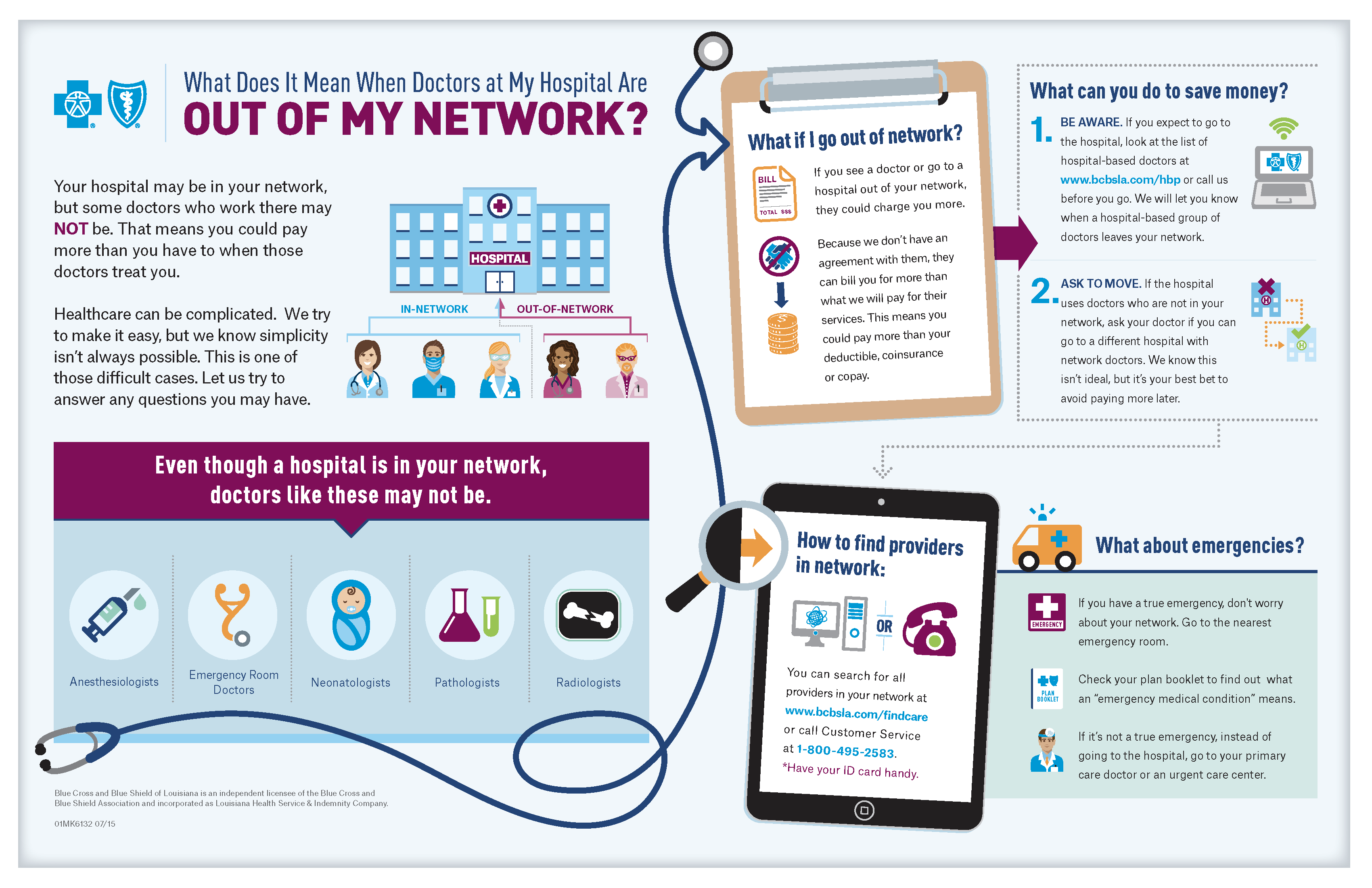

“The thing is, not all of the doctors and healthcare providers working in facilities (like hospitals) work directly for that facility … That means the hospital, clinic, etc., often don’t “own” all the docs roaming their halls.”

Surprise! You’ve Got a Bill

Since nobody can really afford to pay for their own healthcare completely out-of-pocket, we use a third party (insurance company) that pays for the bulk of our care, provided we go to medical providers who are “in network” for our insurance company. This makes getting care in the network a very big deal in terms of keeping your costs in line: You will always pay less when you go to an in-network provider.

Officially called “balance billing,” surprise billing is a bill you get when you go to an out-of-network doctor, hospital, laboratory, urgent care or other healthcare provider. Your insurance plan reimburses the out-of-network provider as much as your plan or the law will allow for your care, and the provider can bill you directly for the difference (balance) between what your plan paid and what that provider charged for your care. Insurance companies negotiate with their in-network providers to set the costs the insurance company will cover and hold the line on what they can charge. That protection disappears when you go out of the network, so the balances for out-of-network services can really add up.

That’s why typically, when we need costly hospital care for a non-emergency, like getting a procedure, surgery or screening done, we go to the hospital or other facility that’s in our insurance network. But sometimes, even after we do our homework and make sure to schedule our medical procedures at an in-network facility (like a hospital), roaming the halls of that hospital are healthcare providers who could have to provide a service to us while we’re there, but are not in our network.

The thing is, not all of the doctors and healthcare providers working in facilities (like hospitals) work directly for that facility.

That means the hospital, clinic, etc., often don’t “own” all the docs roaming their halls. These types of healthcare providers are usually in independent practices and they work for the facilities on contract. That means they don’t have to follow the facility’s payment arrangement with your insurance company.

And for you, it means that while the facilities may be in your network, some medical providers who work there might not be. And, you will likely pay more for having those healthcare providers treat you. Then, when those independent healthcare providers bill you for the services they provided – on top of what you paid to go to the in-network facility for care – that’s “surprise” billing you didn’t know was coming.

I know how it feels because it’s happened to me.

“Well, insurance companies have lots of money, so just make them pay the whole bill the out-of-network doctor charges! What’s the problem?!”

My Surprise Bill

In 2011, I had surgery to replace a worn-out knee, femur and hip, which needed to be done after the cancer I survived way back in 1983. As a Blue Cross employee, I knew better than most customers how important it was to very carefully examine every piece of paper and check that each healthcare provider who was going to touch me at any point during my surgery was in-network for my health insurance plan. After doing that, I felt comfortable that I was covered and that I knew what I could expect to pay out of pocket.

Alas, about a month after the surgery, I got a bill from an anesthesiologist who substituted for the in-network one I had signed up with to knock me out for the surgery. The in-network anesthesiologist got sick the day of my surgery (which I couldn’t plan for or control), so the hospital called an independent one to substitute. This new doc had refused to join Blue Cross’ network (and by the way, I was on the Blue Cross plan with the broadest network of all!) So, because he handled my anesthetic, he sent me an out-of-network bill for more than $4,000. And that was on top of the out-of-pocket costs I’d already budgeted for to pay for my covered, in-network services for the surgery.

Surprise!

Can We Stop the Surprises?

In the interest of consumer protection, many state insurance commissions around the United States are trying to figure out how to hold the consumer harmless so we pay less when this happens. I’m all for that!

And, Blue Cross has worked with our own Louisiana Department of Insurance and our network providers to address the issue of surprise billing for many years. We want to find a solution that’s in the best interest of customers like me, who’ve been badly surprised.

A key problem is that the typical solution offered by everyone except the people who buy and sell health insurance goes something like this:

“Well, insurance companies have lots of money, so just make them pay the whole bill the out-of-network doctor charges! What’s the problem?!”

If you’ve been reading Straight Talk, you can probably point to some of the problems with that. But, to put it Straight, this would take away any incentive for these independently contracted providers to join insurance networks. Why would they commit to following the billing arrangements we have with our in-network facilities if they can just surprise bill at any level they want?

Let’s revisit the whole concept of provider networks. Why do insurance companies have them, anyway?

“But Mike, what if I’m having a true emergency? I’m not going to check the network directory before I have my heart attack!!!”

Networks—What’s the Point?

Probably the biggest consumer protection the average insured patient has is membership in his health insurer’s medical provider networks. These memberships come with three gigantic benefits:

- Pre-Contracted Rates—Every healthcare provider Blue Cross contracts with knows in advance exactly how much he will get paid for every single diagnosis code and procedure he performs and bills for. There is nothing random about the way we pay docs and hospitals because every price is agreed upon up front, documented in our contract with each other. This protects our customers from any out-of-bounds profit seeking or billing errors. In addition, when you pay cash for medical services, before you hit your deductible for example, you get access to the pre-negotiated, discounted prices Blue Cross has made available for you.

- Negotiation Power—All medical providers have a list price for all the services they provide. You may hear the price referred to as a “charge master” or “billed charges” or even a “fee schedule.” You can think of this pricing like the MSRP price on a car. It’s a starting point for negotiations between the insurance company and the medical provider. The final rate we negotiate for our members is typically much lower than that starting point. Our members should be getting a really good deal since there are more of them than any other insurance customers in Louisiana.

- Balance Billing Protection—Every provider who contracts with Blue Cross agrees in writing to hold our insured customers HARMLESS from the difference in prices between his MSRP and the contract rates. So, if a service at your favorite doc has a list price of $100, but the Blue Cross price is $40, then that doctor can never, ever bill you for the other $60. That’s the protection you get for staying “in network.” This is why you should always, always stay in network.

Emergency Arrangements

“But Mike, what if I’m having a true emergency? I’m not going to check the network directory before I have my heart attack!!!”

Agreed. And you shouldn’t. That’s why, in a true emergency, Blue Cross will pay the healthcare providers who treat you like they are in our network, even if they aren’t. We protect our members when they need us. Period.

The problem is, a lot of surprise billing happens for scheduled procedures or treatments for things that are not emergencies. And, just because you go to the ER for care, it doesn’t mean it will be automatically considered an emergency. Read my blog post on lower-cost options to get care outside of the ER for non-emergencies for more on that.

So now, you can see the problem with surprise billing. Inside a medical facility, there might be many providers who treat you, and they might each work for their own companies and not the facility. And, one rogue provider can turn into a gigantic bill that your insurance company will only give you limited (or sometimes NO) help with. Big problem.

How Does Blue Cross Prevent Surprise Bills?

Our hands often get tied in these situations because while we work hard to get hospital-based doctors around the state to join our networks, not all of them choose to do so. And, we can’t force any provider to join our network.

One way we protect our customers from balance billing is to make our in-network hospitals tell us which healthcare providers they contract with – anesthesiologists, emergency room doctors, neonatologists, pathologists, radiologists and others who may not be in our network – and we post this information online to make it easier to see which providers at the places you go for care are in and out of your network. You can check here to find the in-network hospital-based providers at the hospitals you use and view the infographic below on how to watch out for out-of-network providers.

My Solution: Whoever Controls the Keys Runs The Show

Ultimately, the medical facility itself controls who gets in the door to see their patients, and they know which insurance company networks most of their patients are in. Therefore, doesn’t it make sense for the facility to require their medical providers to participate in the insurance networks the majority of their patients use? I mean, even if they did something simple like saying, “All our providers have to be in the Blue Cross PPO network,” which is our largest network, it would eliminate a lot of surprise billing.

Or, they could at least take the “surprise” out of surprise billing by doing as we do and posting their providers online and discussing this with patients scheduling procedures there to warn them that someone outside of their network might end up treating them.

If I were a hospital administrator, I would certainly explore that option. Since almost all facilities accept both Medicare and Medicaid patients, they are already requiring their docs to accept government healthcare programs. Why not require Blue Cross insurance as well?

The last thing we need to do in this case (and it has been suggested) is to force insurance companies to reward bad behavior by paying doctors who won’t join our networks the same rates as the ones who do, which would disable those three key protections I laid out above. Talk about throwing out the baby with the bathwater!

So, whether you call it “balance billing” or “surprise billing” or just a pain in the rear, let’s not get rid of an entire raft of existing, needed consumer protections to solve this problem.

We’re committed to keep working with our providers, state regulators and other stakeholders to find a solution that works for this issue.

The Mississippi Legislature passed a law in 2014 concerning balance billing. It’s on the books today, enforced by our MS DOI. It is § 83-9-5. Mandatory policy provisions. The law says if a provider accepts insurance and files the claim for the patient, they may only bill for deductibles; copays; and coinsurance. This has helped a number of our customers who get the “surprise bill” from the hospital based physician such as anesthesiology; ER physicians; radiologists; etc. It also has helped with ground ambulance service (not air as that is governed by FAA).

Michelle Fuller

Vice President & Advisor

BancorpSouth Insurance Services, Inc.

There is a surprisingly easy way to fix this. I have asked for years to have a CPT code driven platform within ilink blue. Attached to that CPT code could be coverage guidelines, fee schedule, if a lab code could list covered lab entities, (same for anesthesia). Instead BCBS spends a ton of money trying to educate patients on how good they are and how the doctors are the enemy. We spend an inordinate amount of money to verify benefits upfront and give ded and coinsurance amounts. Guess who has the disclaimer saying (not a guarantee of coverage) the insurance company! There would be NO surprises if the benefits verification system was accurate, timely and had the information needed (and guaranteed it!) We spend more money then ever before trying to educate patients and get paid but our reimbursement is at an all time low. I sent an email asking for assistance from my provider rep this week…what I received back was a threatening email because she ASSUMED something. I am not sure why BCBS has taken a hostile approach to their providers but I think it is time for providers to start looking for ways to get this back on track instead of being penalized non stop.

Debbie! We very much appreciate your ideas here! Here’s something for you to think about, if you are dissatisfied with reimbursement levels: In 2004, when I joined BCBSLA, drug spending was about 11% of premiums coming in the door, and physicians/services was almost 30%. Today, drug spending is UP to 26% of premiums. It seems PHARMA is crowding out money we could be spending on other things. Make sure your providers are aware of the REAL prices of the meds they prescribe (not what the copays are) and that will go a long way to re-balancing that problem.

thanks!…mrb

Wow, really hard to find a place to comment. No wonder there aren’t many.

Just heard you on Public Radio Baton Rogue.

A couple of questions.

My Medicare seems to set the prices that they will pay. For instance on the ambulance it was billed at $1500, Medicare paid $350. Hospital room for a couple of days, billed at $5000 or so, Medicare allows and pays a fraction of that, about $500. I can get the actual numbers but close enough.

How do the policies through the ACA handle this. Do they pay the full billing amount for a given service or do they have similar discounts? And if so what are they based on? Put another way, what is the discount that your policy provides? If it’s like Medicare it would take a lot of stuff to reach the $2500 deductible. I just had an ablation and so far the supplement has had to pay about $1000 out of over $30000 of retail billing.

You stated that Medicare has no lifetime caps and that if you were to have cancer say that you could be liable for 80% of a million dollars. But Medicare would only allow an pay a fraction of the total billing. So it’s misleading to say that. A friend of mine’s wife had breast cancer a couple of years ago and the bill was huge. In the end he offered to pay what Medicare would allow and suddenly he easily managed it as it was less than a third of the original billing.

I never hear this discussed in relation to these health plans. I don’t think people understand this and just what they are liable for if uninsured as opposed to insured. It’s a huge difference and very important.

I have friends who tell me they will just pay cash without understanding just what it is they could be getting into.

Only a fool doesn’t want to have some kind of good health insurance policy. And we have a lot of fools but many are just not well informed until they take the ambulance to the ER and get hit with that $1500 and an ER bill for $3000. With insurance it would be much less.

I’m old enough to remember when health insurance companies were mutual companies in which the premium payers were members and any profits went back to the members. Now it’s non-profit and the CEO salaries are ridiculous. The change was supposed to make it better and more “efficient” but now the core mission seems to be to deny care rather than get the bills paid.

There’s more but I can’t think of it right now. I feel the whole story is not being told and if people really understood how the game is being played some big changes would happen.

The Republicans seem to be on the side of maximizing profits, I believe that the profit motive should not be in something like health insurance. The amount of money spent on advertising for clients is huge and that all comes from premiums. That’s healthcare unpaid for.

Thanks for your time.

From: Mike Bertaut, Healthcare Economist:

Wow! Hugh, great questions and I’m sorry it took so long for me to get back with you. Had a few issues with my log-in on the tool, but that’s all fixed now. Let’s get started:

1. ACA policies are built on medical provider networks that have agreed-upon-in-advance rates for every single thing your Doc can do to you (other than experimental stuff). There is nothing random about how insurance companies pay on any policy, let alone ACA stuff.

2. The discounts vary from medical provider to provider. It’s all a negotiation and some docs and hospitals get paid more.

3. Medicare Part A and B do not provide lifetime caps on your out of pocket costs like private insurance does. So if you run up $1m in Medicare-approved expenses and you have no supplement or private wrap-around for your Medicare, you would be on the hook for 20% of that out of pocket.

4. You can rest assured that your BCBSLA plan is a mutual company, owned by the members, and all the money is owned by the members. CEO salary is not a cost driver for us, and represents a very tiny percentage of your premiums (less than 3 one/thousandths of 1%). We run a very lean company and last year, directly and indirectly, almost 90% of all the premiums paid in bought healthcare for someone.

5. You can also rest comfortably in the knowledge that our advertising budget is also very small. We’re not a drug company, where they spend twice as much money on marketing as they do on R/D. That’s not where the money goes.

It’s healthcare, plain and simple. Skyrocketing drug costs, rising inpatient hospital costs, new technology, and an unhealthy population all contribute to the problem. But it’s healthcare, not the other stuff you mentioned, that is driving up your premiums.

mrb

I am a medical provider. If balance billing is removed, the provider would have absolutely no say in the reimbursement rates. The insurance companies have already decreased reimbursement dramatically over the years, there would be nothing from stopping them from reducing reimbursement even further after eliminating provider recourse. Unfortunately since provider appeals to insurance companies for incorrect or low payment are an auto fo futility, the only way for providers to get the ear of the insurance company is to have the patient contact the insurance company to resolve the issue. Patients become motivated to become involved generally only under the circumstance that they are billed from a provider for lack of payment from their insurer. If we give all the power to determine pricing to the payor I’m quite sure that the insurance companies would be pleased with that outcome. The providers on the other hand, not so much. To try and force providers into accepting reduced rates is unacceptable and quite frankly a gross misuse of a well intended patient protection effort.

Julia!

Thanks so much for reading Straight Talk! I completely understand your frustration about reimbursement rates, and I’m greatly concerned myself that the pharma spend is crowding out the “human spend” in healthcare. IN fact, when I started with BCBSLA in 2004, we spent 11% of premiums on prescription drugs, and 33% of premiums on Docs/Specialty care and outpatient services that they prescribed.

In 2019, those numbers are now 28% pharma, and 22% Docs/Outpatient care!! Essentially, the prices of the drugs medical providers are prescribing are crowding out their own ability to make more money. That’s why we’re pushing Quality Blue Primary Care so hard, it really allows a provider to take back control of their own financial destiny by improving the health of their population. A concerted effort to get behind QBPC and increasing provider awareness of the REAL price of the drugs they prescribe are the best ways to make more money available to address your concerns.

As far as “balanced billing” is concerned, I don’t know of anyone seeking to eliminate a provider’s choice to join, or not join any insurance company network. What is a concern for us is SURPRISE billing, which happens when the provider doesn’t make the consumer aware of their lack of network status, or give the consumer a choice to say “no” to a non-network provider. Since there are providers that build their entire business model around this ability to mask their status, and something like 20% of all claims nowadays involve out of network billing, to keep insurance prices from climbing faster we need a solution that automates that process, like when disputes occur, a provider getting paid a % of Medicare or some other index. To do otherwise will drive a ton of administrative cost into the system. Like in NY today where every disputed claim is costing $400-$600 EACH in additional administration/arbitration fees on TOP of the claim itself!

Thanks for hanging in!…..mrb