This year marks the 21st year that I’ve been deeply involved in how healthcare is financed in Louisiana, seeing how money moves through that system. I’m surprised at how many moving parts and different players are involved in delivering and paying for healthcare.

As a nation, we now spend 20% of our Gross Domestic Product (GDP) on healthcare. You can think of GDP as the dollar value of everything our country produces; all the goods and services. GDP of 20% on healthcare means $1 out of every $5 on EVERYTHING our nation produces is spent on the administration, delivery or financing of healthcare.

That’s a big deal. $1 out of every $5. No other country comes close to this.

Let’s localize that a bit and talk about how Louisiana Blue spent over $5 billion in the hard-earned money you trusted us with during 2025. Where did your $5+ billion in premium payments go?

The Straight Talk: 2025 was a hard year for Blue Cross and Blue Shield Plans nationwide, and Louisiana Blue was no exception. We lost more than $177 million on our operations in 2025.

We responded to this and reduced our workforce over the course of the year through a combination of letting open positions go unfilled and making much more difficult decisions to reduce staff (that’s jobs lost that were based here in Louisiana!) and budgets.

The hard question remains: Why did we lose so much money?

Medical costs, along with the volume of healthcare services and prescription drugs our members used, went up faster than we expected. Almost historically faster. Drug costs continued to skyrocket in the past year, with a spending increase almost double what we expected. That big of a shock is not really something you can plan for ahead of time.

For the rest of the story, let’s look at where our members’ 2025 premium dollars were spent.

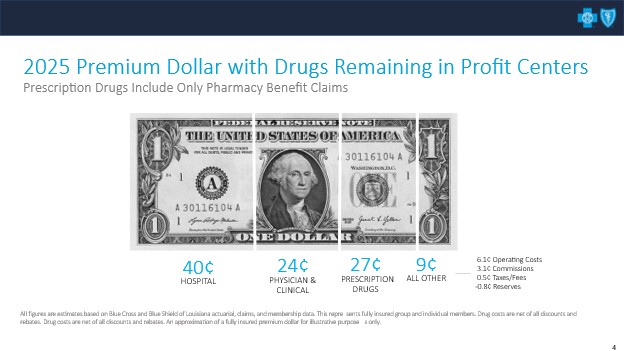

2025 Premium Dollar Breakdown By Numbers

As you look over this spending breakdown, remember that the totals for hospitals and physicians/clinical also include some prescription drug payments. Costs and profits for providing these drugs for hospitals, health systems and other providers are retained in the category (hospital, physician/clinical) where the drugs were delivered. If you got medicine in the hospital, those costs went into the “hospital” bucket. If you got an infusion of drugs at your doctor’s office, those costs are in the “physician and clinical” bucket. All the drugs picked up at a pharmacy or delivered via a mail-order pharmacy are included in the “prescription drugs” category.

You can see that for each premium dollar members paid Louisiana Blue in 2025, on average:

- 40 cents went right back out to pay a hospital or hospital-owned facilities

- 24 cents went to outpatient services like doctor or specialist visits, labs, imaging, rehab, etc.

- 27 cents went for prescription drugs picked up at a pharmacy or delivered via mail order

- We ran all of our business operations on 9 cents of each premium dollar, which includes salaries for almost 2,500 hard-working Louisianians. Part of the 9 cents is also regulated, meaning there are some parts of our business, such as products we sell under the ACA, that prohibit us from keeping more money for operations.

When I say “operations,” I also mean things like taxes, broker/consultant commissions, IT upgrades, complying with state and federal regulations, insurance and keeping our regional offices up and running.

You may notice the reserves contribution was negative for 2025. That’s because we had to take money out of our rainy-day fund to operate. And that can cause some significant problems.

Our rainy day fund has helped us through difficult times, making sure we are able to continue paying for medical claims and reimbursing providers during natural disasters or other difficult times. In the aftermath of hurricanes Katrina and Rita, and more recently hurricanes Laura and Ida, Louisiana Blue was able to use our reserves to cover millions of dollars in payments to Louisiana hospitals and doctors – even though our members in the affected areas were not able to pay their premiums on the regular schedule. It’s scary to head into hurricane season knowing we have not been able to build up our safety net as usual.

It’s part of our job to show our regulators that our business model is sustainable. Since we are a not-for-profit company without shareholders, we can’t just issue stocks and bonds to raise money when we run short. We have to maintain the discipline of a rainy-day fund to tide us over until we start breaking even again.

Waiting to break even also means rate increases, which we unhappily had to do for 2026. But as I’ve written about before, the more it costs to provide medical services, the higher rates must go to cover those costs. If accelerating medical costs don’t slow down, we’ll have to do it again in 2027. Nobody wants that.

Why 2026 Is The WRONG YEAR to Come Asking for More

An ongoing real-world pressure on your rates are the constant demands we receive from large healthcare systems and provider organizations — typically from the executive leadership and negotiating teams — to increase their reimbursement for the same services.

To be fair, we have plenty of good providers in our networks who understand healthcare cost challenges. Those providers negotiate in good faith and genuinely try to solve problems with us. They add value and join us in our mission to improve the health and lives of Louisianians. We work with providers through our Quality Blue programs to make sure our members are getting the right care, in the right settings at the right time. Quality Blue providers have worked with us for over a decade, and the programs actually do improve outcomes and reduce cost growth. Providers can even earn higher payments by keeping their patients healthy and out of the hospital.

The problems and the cost increases come with the “pay us more” medical groups. As I’ve shared before, the government healthcare programs (Medicare and Medicaid) reimburse providers at significantly lower rates than private insurance. Without the payments from Louisiana Blue, many providers who see Medicaid and Medicare patients would have to see fewer of them or go out of business. Even though their problem is with government reimbursement, they come to us (to YOU, our members and our employer groups!) to make them whole.

Unfortunately, our ability to subsidize those government programs has hit a wall. We are already losing money. That is not a theory — it was the 2025 result, as illustrated in that dollar bill graphic.

Increasing provider payments without justification through a significant improvement in outcomes or higher patient volume causes higher costs. And those increased costs get passed along to families, small businesses and retirees who are trying to make payroll and buy groceries.

So here’s the Straight Talk: Our premium dollar is already spoken for.

If a provider organization comes to us in 2026 saying, “We need a big increase,” without regard for quality, our response is simple – “At current rates, we lost money. At current utilization, 91% of our members’ premium dollars already go straight to their medical care and drugs. This is not the year for cost increases — it’s the year for cost discipline.”

In 2026, higher payments must be earned through measurable improvements in outcomes, efficiency or access — not simply higher prices for the same care delivered in the same way.

Our members and their patients cannot afford to spend more of their income on these providers.

Leave a Reply